Young people have many financial difficulties.

Housing is expensive. Student loans. Inflation. Cost of daily maintenance. etc. etc.

I know there is disillusionment and concern about financial nihilism among Gen Z, but I trust young people.

This group has already figured some things out.

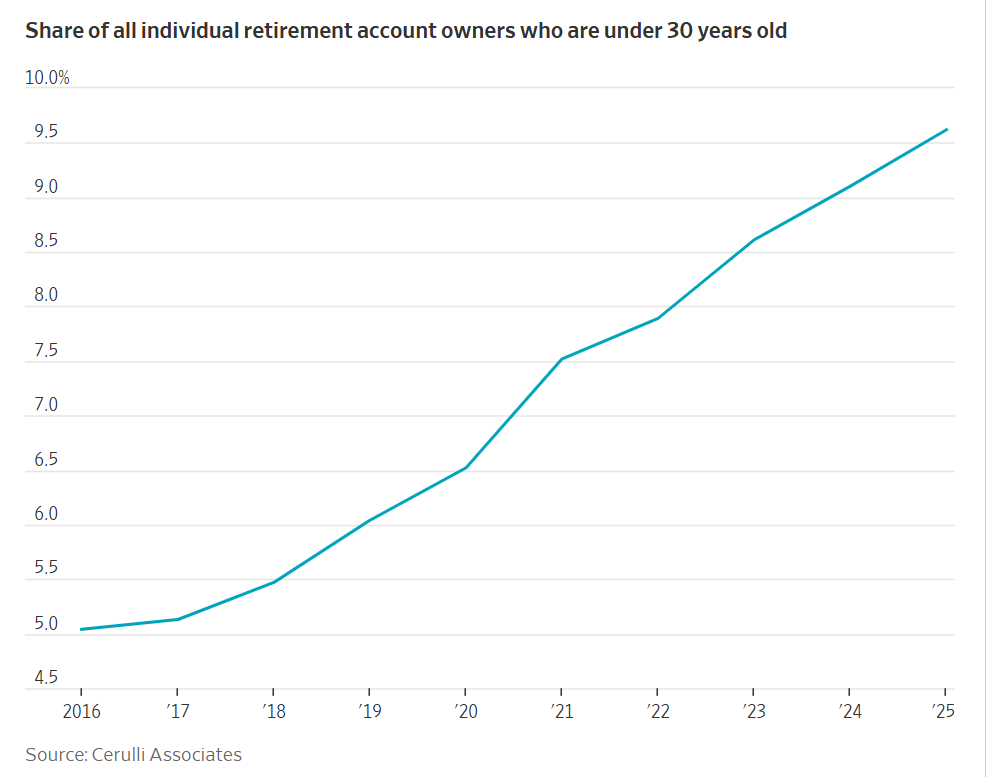

Wall StreetJournal It shows that people under 30 benefit from tax-deferred retirement accounts:

The share of IRA accounts held by those under 30 has nearly doubled in the last 10 years.

Here’s some more data:

Total IRA contributions among Gen Z investors increased 65% year over year in the first quarter of 2026, compared to 31% for Millennials. According to Fidelity Investments, three-quarters of people 35 and under choose Roths, compared with less than half of those in that age group a decade ago.

This is great news!

Young people are saving and investing for their future. If they don’t stop compounding in these accounts, the wealth will be spectacular decades from now.

The great thing about qualified retirement accounts is that they are excellent vehicles for long-term investments like stocks!

Young people have developed a taste for stocks.

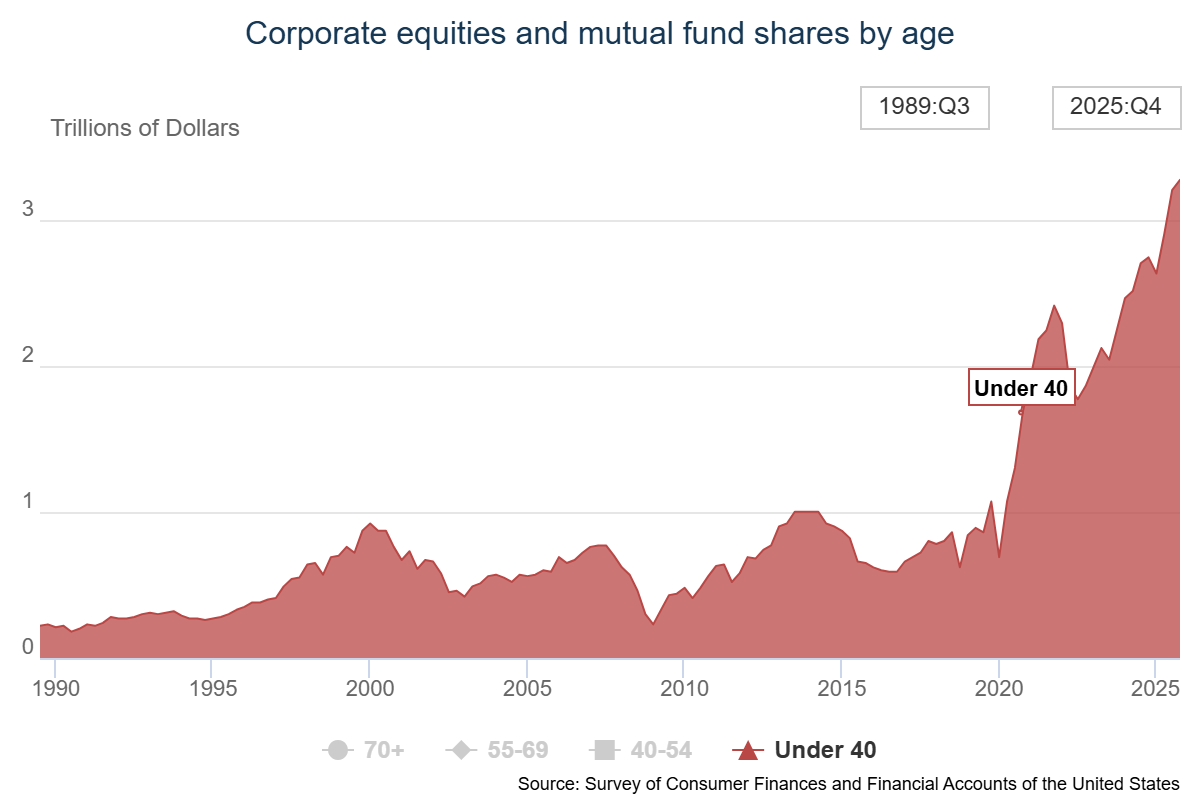

Look at the change in the value of stocks owned by people under 40:

It has increased 3 times since 2020. The share of stocks owned by people under 40 is still relatively low (6%), but it has doubled in the decade.

This is progress.

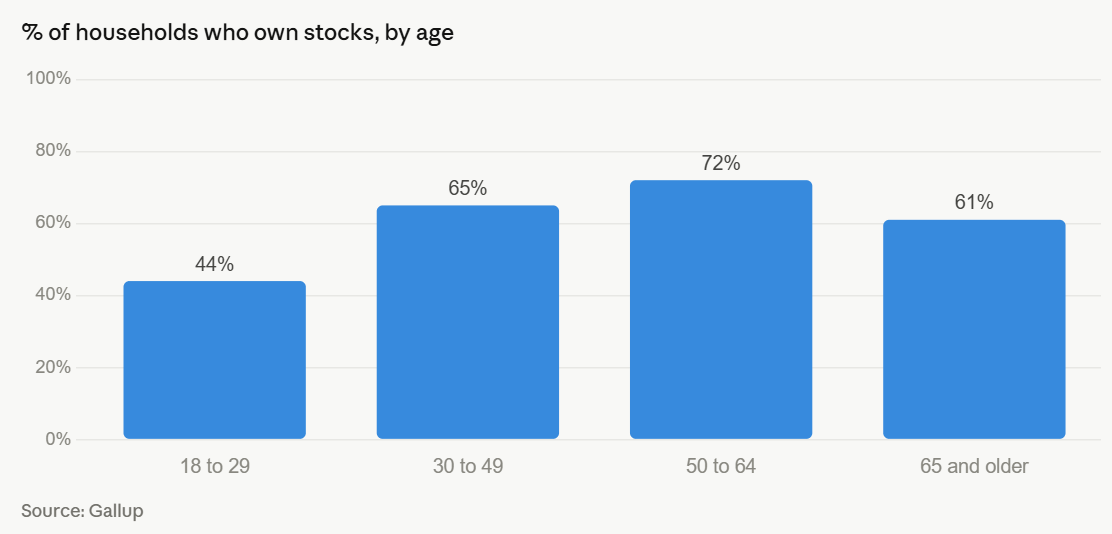

Here is the distribution of household stock market ownership by various age groups:

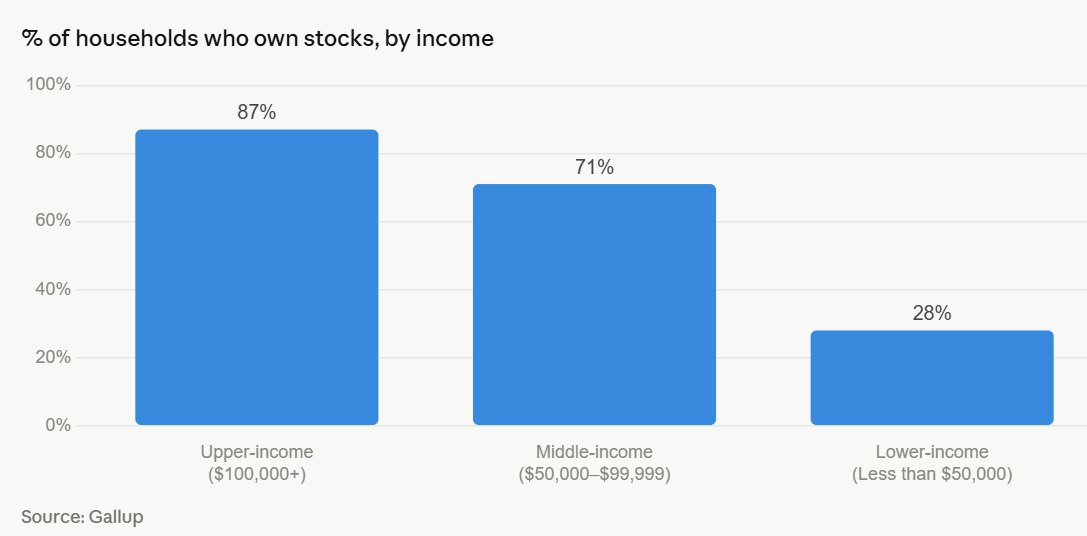

Now here is by income level.

If you want to take a glass-half-empty perspective on the world, you could say that younger households and lower-income households (which have a lot of overlap) have much lower levels of ownership than older people and those with higher incomes.

This is of course true.

But these numbers require context.

I wrote a whole chapter Risk and Reward About the history of stock market ownership in America.

In the early 1950s, only 4% of households owned any form of stock. In the early 1980s, this rate was only 19%. Things didn’t really get better in terms of mass buying of stocks until the 1990s.

From a glass-half-full perspective, young and low-income households own more stocks than the entire country at that time. The numbers are moving in the right direction top 10% still owns most of the shares.

Of course, one reason why more young people are investing in the stock market is that housing is so expensive. Unless you’re building equity in a home or saving for a down payment, there’s more disposable income available to invest in stocks.

But it’s also about a fragmentation barriers to entry in financial markets.

Technology makes investing easier. Wages have fallen. Minimums do not exist. Investors are more conscious.

We need more people investing in the stock market. The sooner the better.

This is great news for young people.

Further Reading:

Are Young People Going Crazy?

This content containing security-related opinions and/or information is for informational purposes only and should in no way be relied upon as professional advice or endorsement of any practice, product or service. No guarantee or warranty can be given that the views expressed herein will apply to any particular case or circumstance and should not be relied upon in any way. You should consult your own advisors on legal, business, tax and other related matters regarding any investment.

The comments contained in this “post” (including any associated blogs, podcasts, videos, and social media) reflect the personal opinions, perspectives, and analyzes of Ritholtz Wealth Management employees making such comments and should not be considered the opinions of Ritholtz Wealth Management LLC. or its respective affiliates or a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any security or digital asset or performance data are for illustrative purposes only and do not constitute investment advice or an offer to provide investment advisory services. The tables and graphs contained therein are for informational purposes only and should not be taken into account when making any investment decisions. Past performance is not indicative of future results. The content speaks only from the date specified. Any projections, estimates, estimates, targets, expectations and/or opinions expressed in these materials are subject to change without notice and may differ from or contradict views expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives compensation from various organizations for advertising on affiliate podcasts, blogs and emails. The inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or Ritholtz Wealth Management or any of their employees. Investments in securities involve the risk of loss. For additional advertising disclaimers, see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see the descriptions Here.