In my opinion, there have been two major changes in the asset management field in the last 20-30 years.

First, financial advisors have moved from selling products to offering holistic, goal-based financial advice.

Second, most advisors have given up on the idea of seeking alpha as a way to provide value to clients.

This is not the entire industry. There are still products for sale. People are still looking to outperform the market.

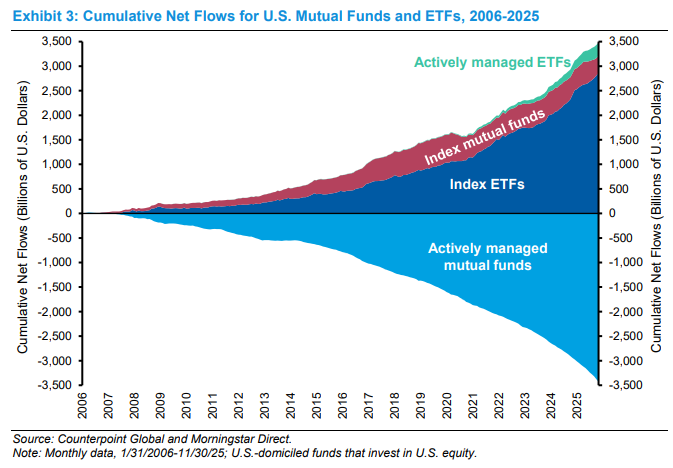

But for all intents and purposes, indexing has won out over active management (via Morgan Stanley):

So what’s next?

I’m sure AI will have something to say in the coming years, but the biggest trend I’ve witnessed firsthand in recent years is the desire for tax alpha. Most clients and advisors recognize that it is difficult to beat the market and that there is no consistency in superior performance.

If you want to add value, it’s much easier to focus on the things you can control, like fees, asset allocation, withdrawal strategies, financial planning, and taxes.

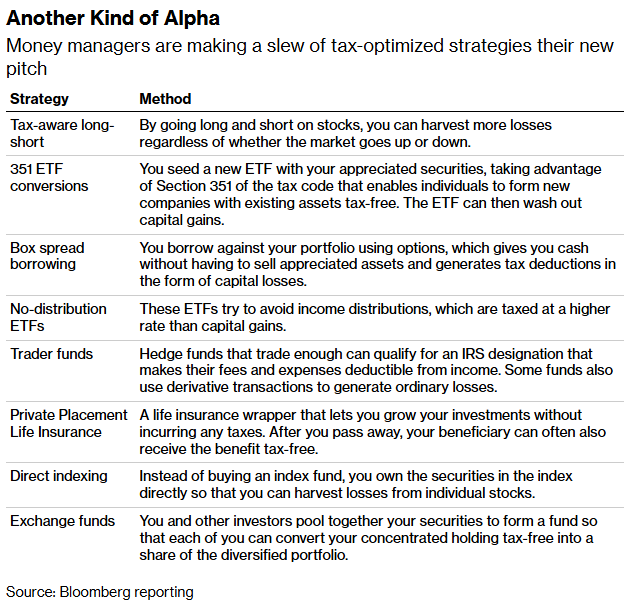

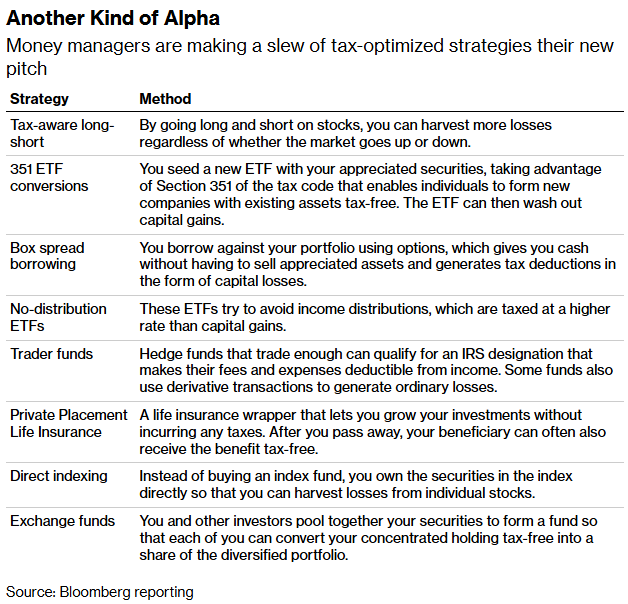

Bloomberg recently had a long profile on how popular tax alpha is in wealth management.

Investors have always valued tax efficiency, but there have never been more options at hand when it comes to managing taxable portfolios:

If you are not in the wealth management field, you may not be familiar with many of these strategies.

Some have been around for years. Others are relatively new and have rapidly become more popular due to improving technology and lower trading costs.

Speaking from experience, the popularity of these strategies is rapidly increasing. We ensure that our customers come to us to find these solutions.

Typically, they are clients who have made large gains from concentrated stock purchases, funds they hold long-term, or capital gains from another transaction (sale of a business, real estate, stock options, etc.).

People are well aware that what matters most is your net returns (the amount you take home after tax).

Tax loss harvesting, either directly or through private indexing, has received the most attention this decade, but this is now expanding to include 130/30 funds, 351 exchange funds, foreign exchange funds and the like.

Many investors consider taking losses to offset gains elsewhere, diversifying their portfolios from concentrated positions, and generally deferring paying taxes on gains for as long as possible to avoid interrupting the compounding process.

I am of the opinion that the tax tail should not always wag the portfolio dog. Most of the time, you shouldn’t make investment decisions based solely on tax efficiency. But it’s truly surprising how many tax-efficient strategies there are these days that add value on top of what you’re trying to do with your client portfolios.

Solutions are getting better and better.

We use many of these tools to: Ritholtz Wealth. One of our partners is O’Shaughnessy Asset Management. We have been using Canvas’ proprietary indexing platform since day one, and the tools have provided tremendous added value to the financial planning process.

Last week I spoke with Ehren Stanhope from OSAM. Talking About Wealth To discuss:

- Difference between direct indexing and custom indexing.

- How can long/short funds help you lower your tax bill?

- Balancing complex and simple portfolio solutions.

- How can we turn highly valued stocks into a more diversified portfolio?

- The role advisors play in tax-managed strategies and more.

Watch the full conversation here:

Or listen to the podcast version here:

Subscribe to our Talking Wealth Newsletter Here.

Further Reading:

Why Are Rich People Still Borrowing?

This content containing security-related opinions and/or information is for informational purposes only and should in no way be relied upon as professional advice or endorsement of any practice, product or service. No guarantee or warranty can be given that the views expressed herein will apply to any particular case or circumstance and should not be relied upon in any way. You should consult your own advisors on legal, business, tax and other related matters regarding any investment.

The comments contained in this “post” (including any associated blogs, podcasts, videos, and social media) reflect the personal opinions, perspectives, and analyzes of Ritholtz Wealth Management employees making such comments and should not be considered the opinions of Ritholtz Wealth Management LLC. or its respective affiliates or a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any security or digital asset or performance data are for illustrative purposes only and do not constitute investment advice or an offer to provide investment advisory services. The tables and graphs contained therein are for informational purposes only and should not be taken into account when making any investment decisions. Past performance is not indicative of future results. The content speaks only from the date specified. Any projections, estimates, estimates, targets, expectations and/or opinions expressed in these materials are subject to change without notice and may differ from or contradict views expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives compensation from various organizations for advertising on affiliate podcasts, blogs and emails. The inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or Ritholtz Wealth Management or any of their employees. Investments in securities involve the risk of loss. For additional advertising disclaimers, see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see the descriptions Here.