I still vividly remember hitting all-time highs for the first time since the 2008 crash.

The stock market peaked in October 2007 before entering the Great Financial Crisis. Those were terrible times.

These highs were not broken again until the spring of 2013.

When this finally happened, many investors were worried that these new highs would be temporary. How can you blame them?

These bad events were limited to the two biggest crashes in stock market history. New peaks were few and far between, and everyone was afraid of another peak before they fell off the cliff.

There have been a number of corrections and bear markets since then, but there have also been many new highs.

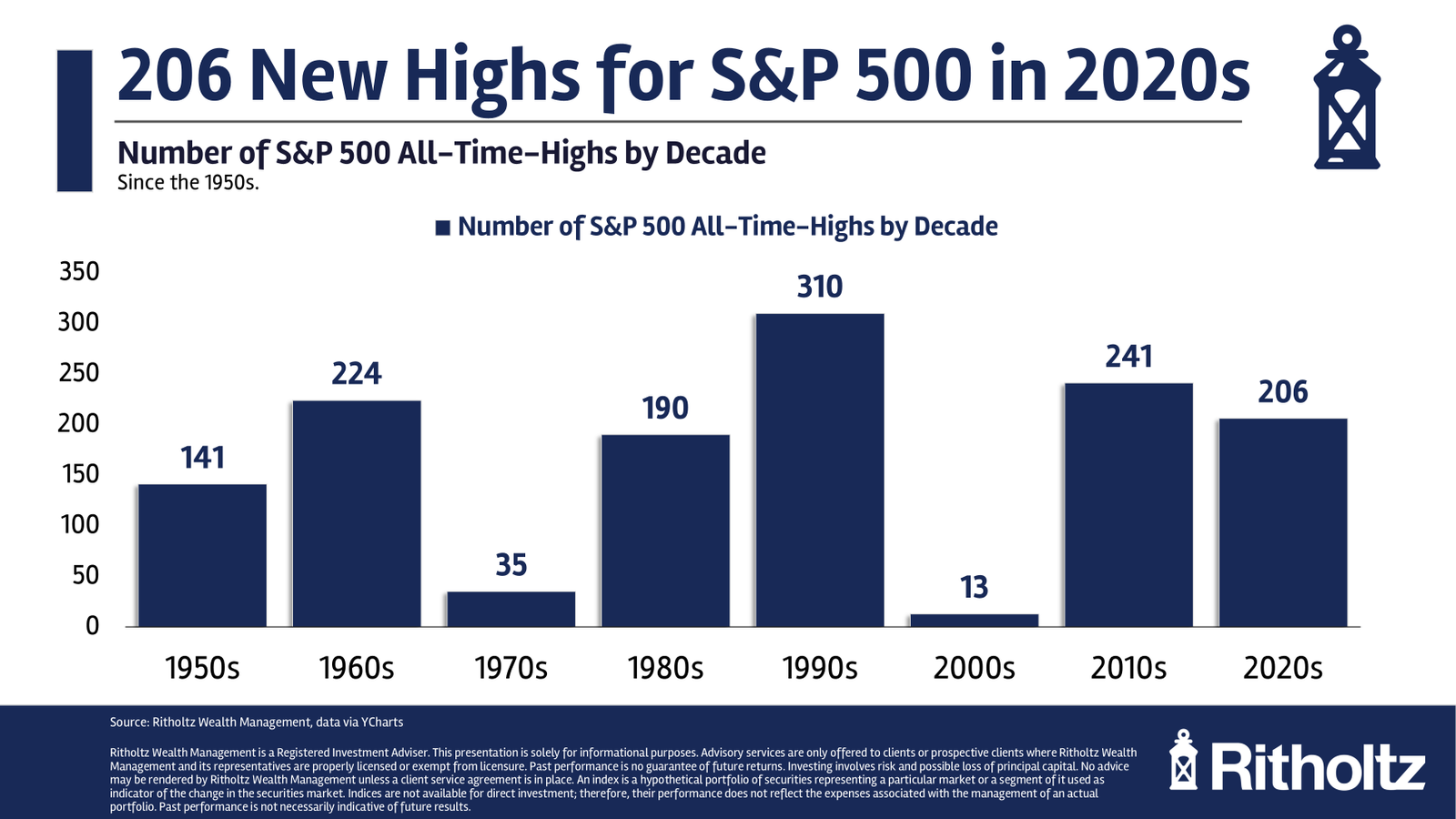

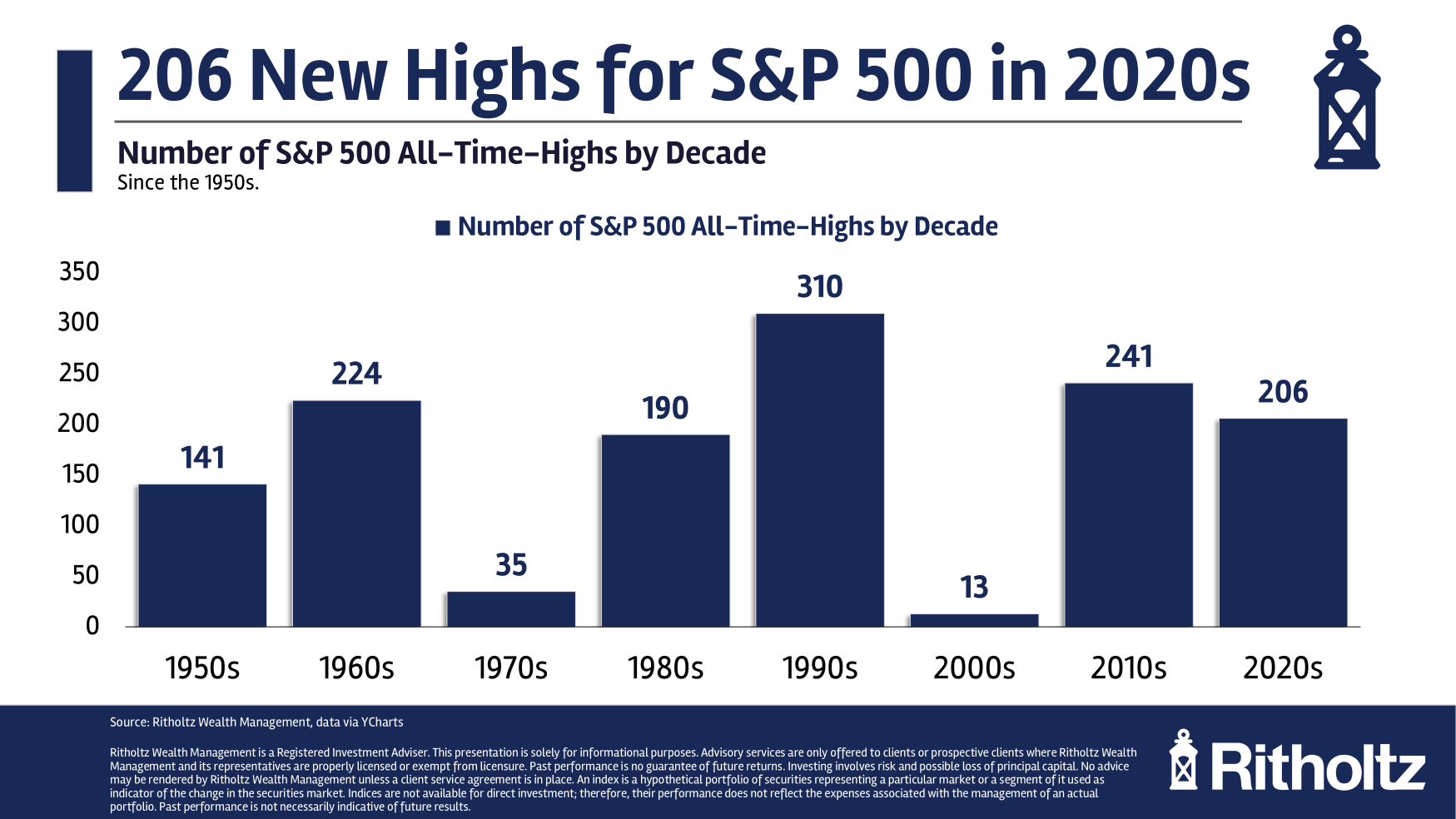

Take a look at all-time highs over the decade, dating back to the 1950s:

The paucity of new peaks in the 2000s was followed by a large number of record peaks in the last two decades. This is a similar pattern that investors saw when the terrible 1970s were followed by the great 1980s and 1990s.

In fact, the current bull market is approaching the number of new highs we saw in that rise.

From the early 1980s through the peak of the dot-com bubble in the spring of 2000, there were 505 new all-time highs.

There have been 447 new peaks since 2013. this is really an epic bull market Run, we’re starting. And the 2020s are starting to resemble the Roaring 20s.

Since 1950, roughly 7% of all trading days have occurred at all-time highs. The highest percentage of trading days reaching new highs in a decade was in the 1990s, at 12.3%.1

This decade isn’t over yet, but we’ve had new highs in the S&P 500 on 13% of trading days.

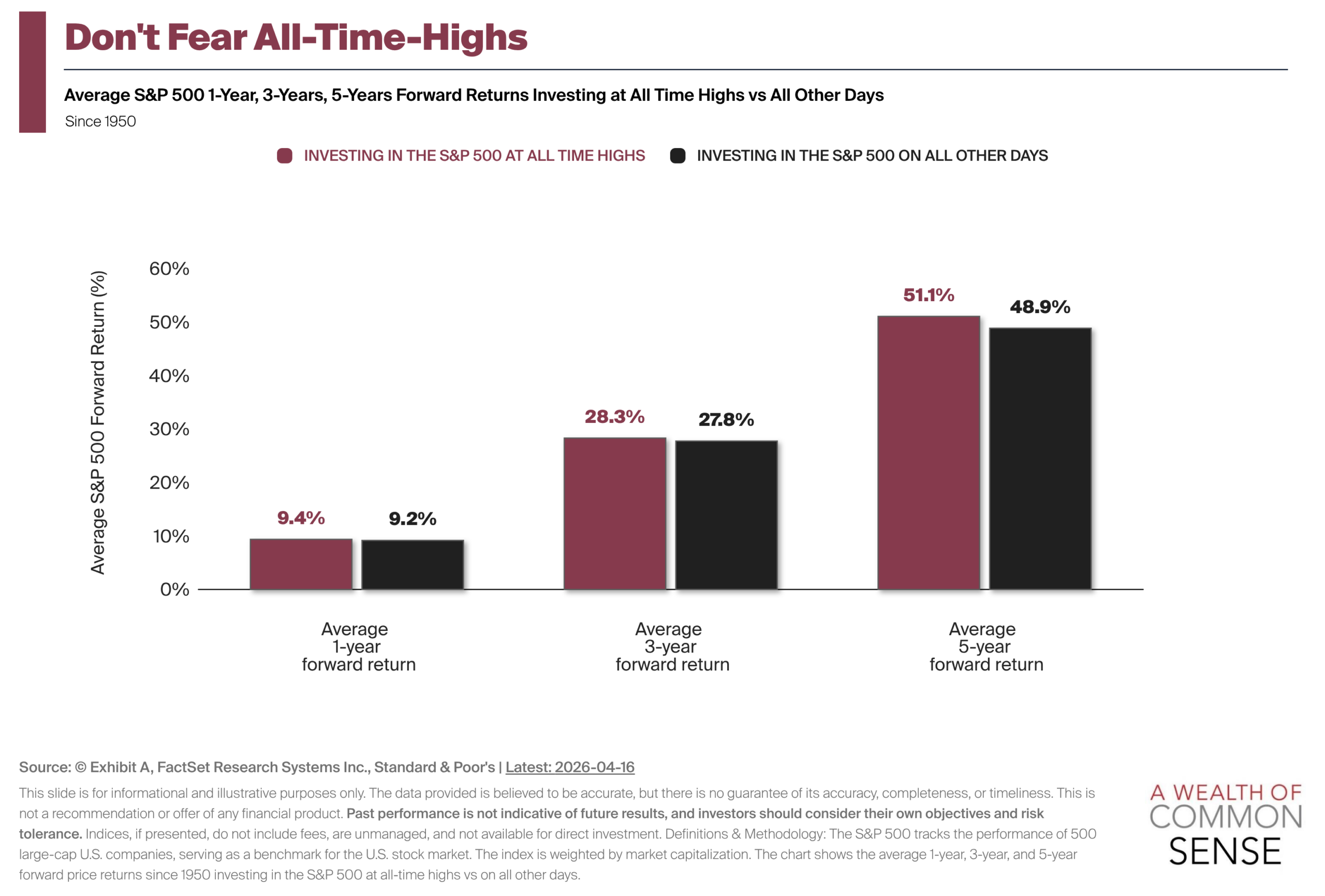

One of my favorite counterintuitive charts shows that average returns tend to be higher from all-time highs than on all other days in the market (via Annex A):

But these numbers make more sense when you consider that new highs tend to cluster in big, beautiful bull markets.

Despite everything that’s happened this year, the S&P 500 hit 7 new all-time highs.

Eventually one of these highs will become the TOP high, followed by a face-melting crash.

But it’s important to remember that new highs are often not a bad thing.

They occur especially frequently during bull markets.

If you are a long-term investor, all-time highs are perfectly normal and nothing to be afraid of.

Further Reading:

An Epic Bull Market

1Surprisingly, the second best percentage is not the 1980s (7.5%), but the 1960s (9.0%).

This content containing security-related opinions and/or information is for informational purposes only and should in no way be relied upon as professional advice or endorsement of any practice, product or service. No guarantee or warranty can be given that the views expressed herein will apply to any particular case or circumstance and should not be relied upon in any way. You should consult your own advisors on legal, business, tax and other related matters regarding any investment.

The comments contained in this “post” (including any associated blogs, podcasts, videos, and social media) reflect the personal opinions, perspectives, and analyzes of Ritholtz Wealth Management employees making such comments and should not be considered the opinions of Ritholtz Wealth Management LLC. or its respective affiliates or a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any security or digital asset or performance data are for illustrative purposes only and do not constitute investment advice or an offer to provide investment advisory services. The tables and graphs contained therein are for informational purposes only and should not be taken into account when making any investment decisions. Past performance is not indicative of future results. The content speaks only from the date specified. Any projections, estimates, estimates, targets, expectations and/or opinions expressed in these materials are subject to change without notice and may differ from or contradict views expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives compensation from various organizations for advertising on affiliate podcasts, blogs and emails. The inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or Ritholtz Wealth Management or any of their employees. Investments in securities involve the risk of loss. For additional advertising disclaimers, see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see the descriptions Here.