Households have dealt with many economic obstacles in the 2020s.

First, there was the pandemic, which disrupted supply chains and led to unthinkable amounts of government spending to keep people and businesses afloat.

This led to the highest levels of inflation in four decades.

Later, the Russia-Ukraine war caused gas prices to skyrocket.

We had tariffs to deal with last year too.

This year’s Iran war has caused gas prices to rise once again.

All told, prices are currently about 30% higher than prices this decade. This is already higher than the price increase of approximately 19% in the entire 2010s.

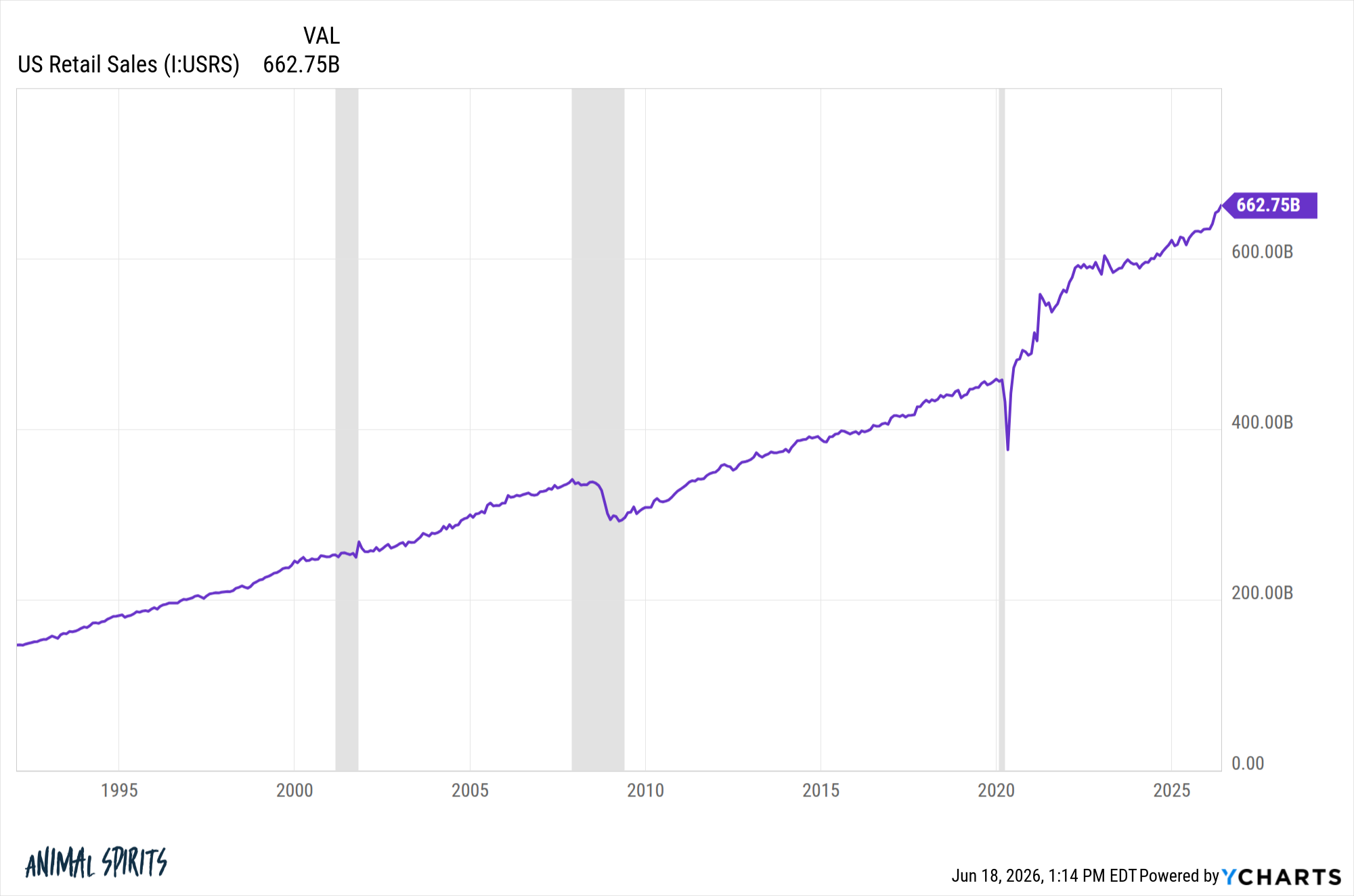

And yet… people continue to spend money:

Despite many predictions to the contrary, there has been no recession since the mini-Covid crisis.

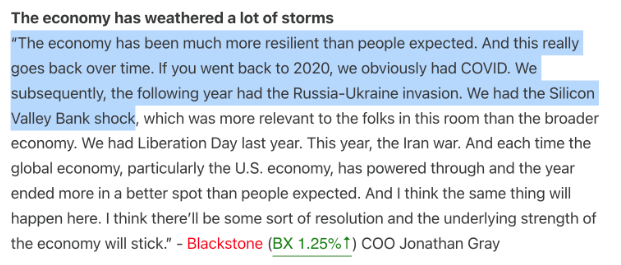

CEOs continue to report on how strong the consumer remains (via) transcript):

Frankly, it helps that financial assets have increased significantly this decade. The wealth effect has certainly been a factor here.

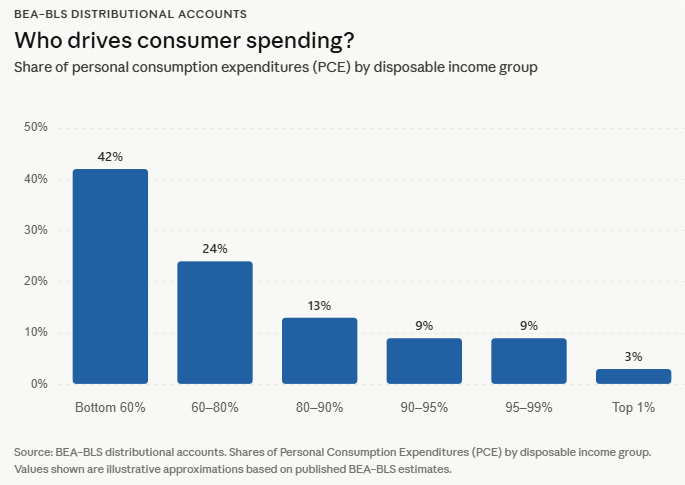

There has been a lot of talk about a K-shaped economy but incoming data BEA It shows that the media spending is not as unequal as you might think:

The real K-shaped part of the economy might be the housing market.

The homeownership rate in this country in 2020 was 65% (roughly at today’s level). At that time, housing prices were much more affordable and 30-year mortgage interest rates were around 3 percent.

If you bought or owned a home before 2022 and took advantage of ridiculously low mortgage rates, you’re locked in the inflation hedge of the century.

Many people have done just that.

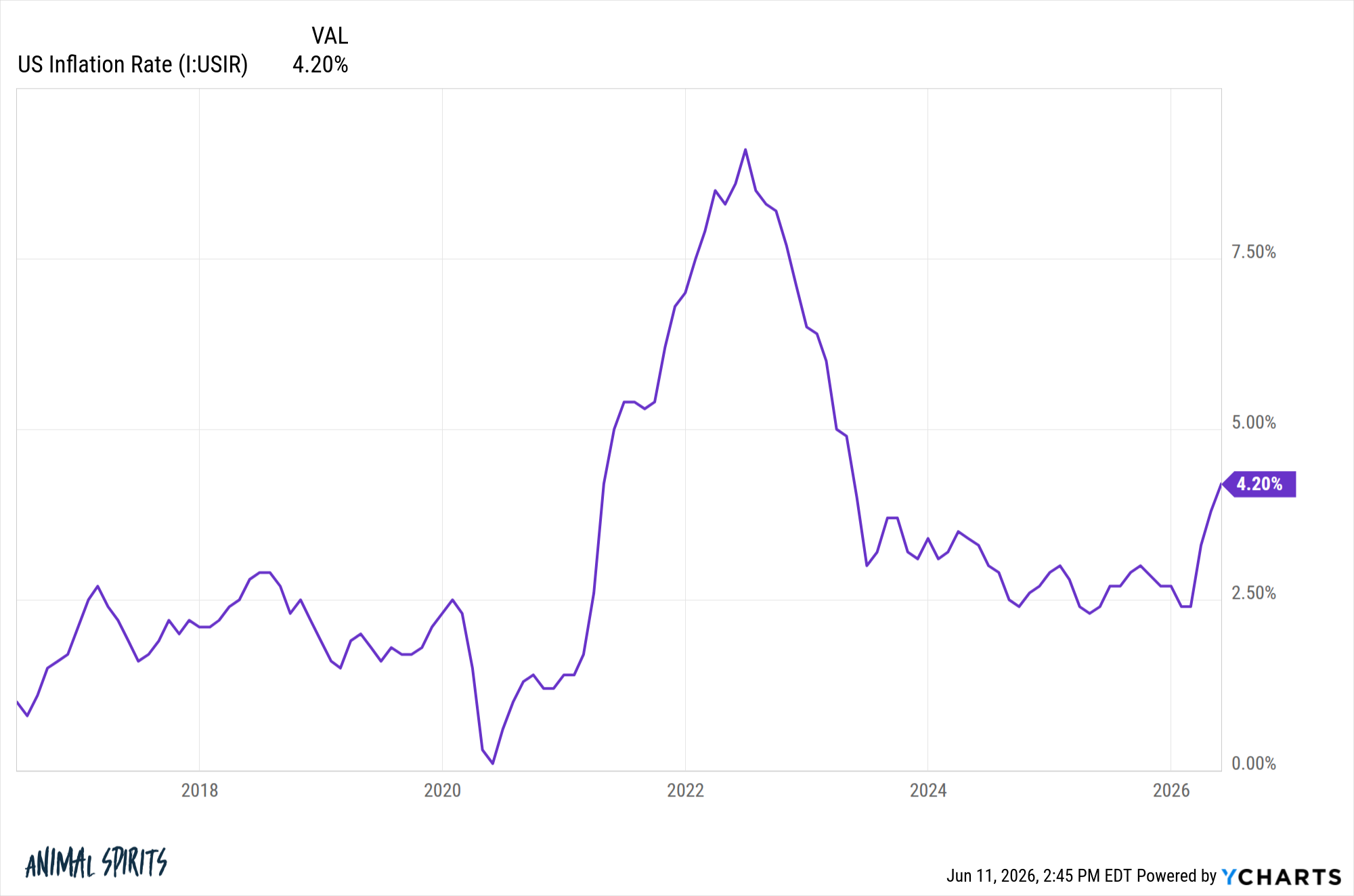

Now look at the inflation rate:

It rose above 4 percent again due to the resilience of the economy and the war in Iran. If you still have a 3% mortgage, you’re now borrowing effectively free on an inflation-adjusted basis.

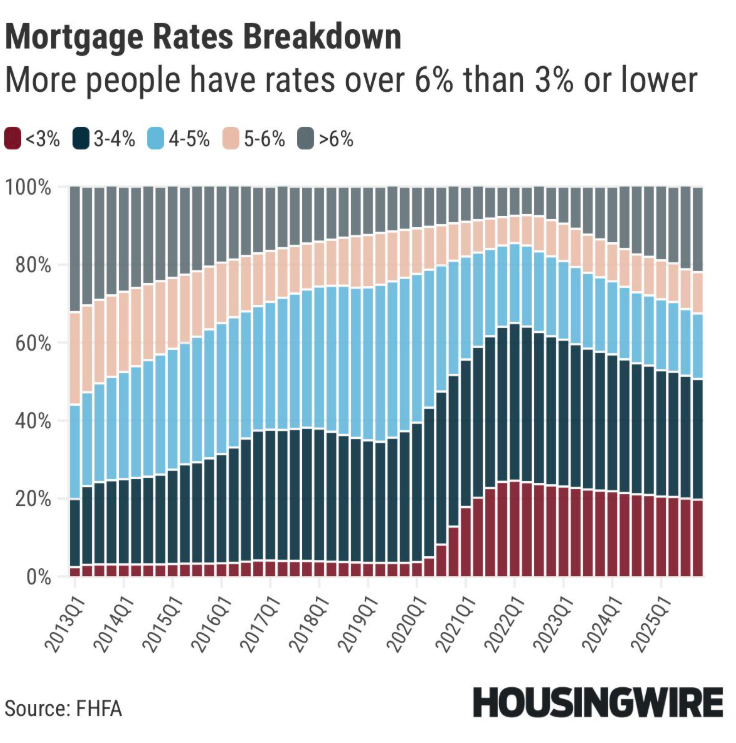

There has been some housing activity in recent years, but they still account for roughly half of all borrowers with mortgage rates of 4% or lower:

When you combine this data with the fact that 40% of homeowners own their home for free, it’s no surprise that households can continue to spend.

How many people can afford to buy their own home at current prices and mortgage rates?

The fact that so many people are stuck with low mortgage payments benefits the economy for a decade.

Money not spent on housing can be spent elsewhere in the economy. That’s why retail sales numbers are so strong. This is also one of the reasons why flows into the stock market continue.

Most economic predictions turned out to be wrong this decade, in part because so many people were able to hedge their biggest budget item.

The real question is: When will this hedge start to fade?

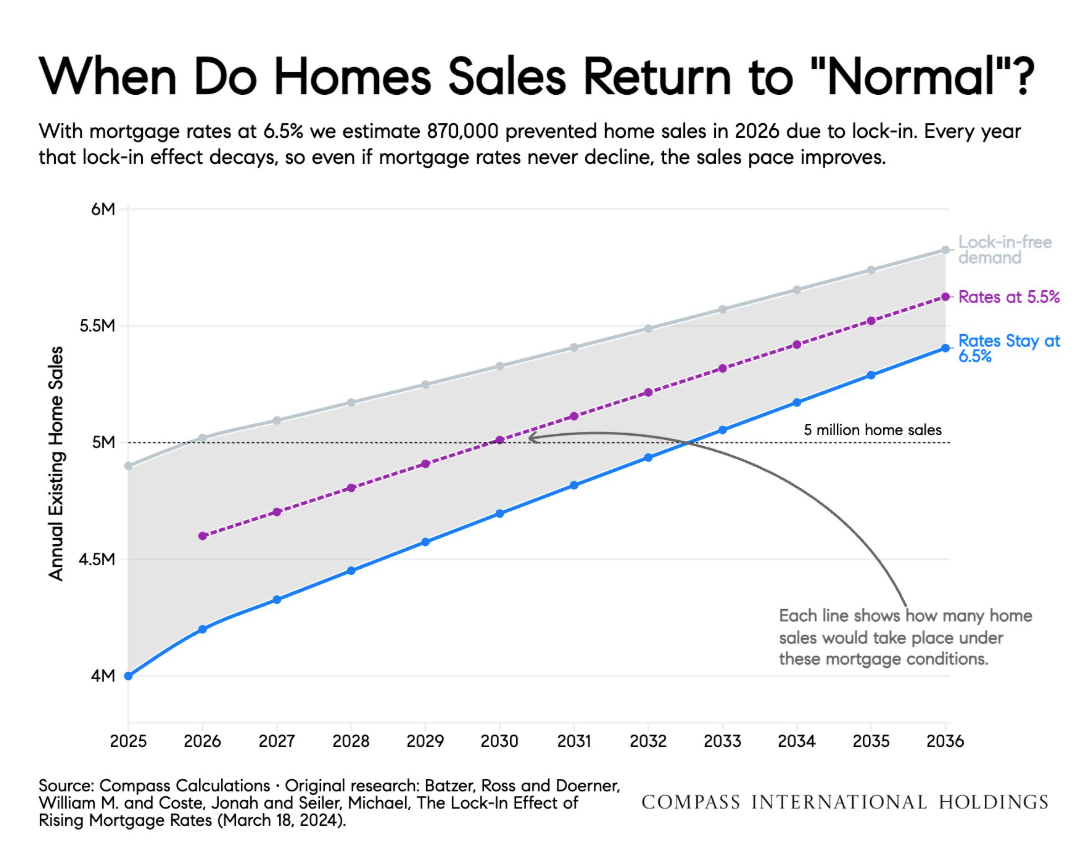

Mike Simonsen He addressed this issue from the perspective of housing activity:

It may take some time.

Of course, crazy things have been happening in housing throughout the 21st century.

The 2000s started with the housing bubble.

When it exploded, we had one of the biggest housing collapses in history.

Prices were extremely affordable throughout the 2010s.

The pandemic has highlighted a tremendous amount of demand and price growth.

So, perhaps there may be an external shock that will change the course of housing prices once again.

The hardest thing about the housing market for many people is that it depends on timing and luck.

Many households have lucked into lower prices and mortgage rates; These came together to protect their lives from risk.

Others were not so lucky and now have to struggle with lower supply, higher borrowing rates and much higher prices.

Michael and I talk about mortgage rates, inflation, consumer spending and much more in this week’s Animal Spirits video:

Subscribe Compound so you won’t miss any episode.

Further Reading:

How Can Consumers Still Spend This Much?

Now here’s what I’ve been reading lately:

Books:

Podcast book tour:

This content containing security-related opinions and/or information is for informational purposes only and should in no way be relied upon as professional advice or endorsement of any practice, product or service. No guarantee or warranty can be given that the views expressed herein will apply to any particular case or circumstance and should not be relied upon in any way. You should consult your own advisors on legal, business, tax and other related matters regarding any investment.

The comments contained in this “post” (including any associated blogs, podcasts, videos, and social media) reflect the personal opinions, perspectives, and analyzes of Ritholtz Wealth Management employees making such comments and should not be considered the opinions of Ritholtz Wealth Management LLC. or its respective affiliates or a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any security or digital asset or performance data are for illustrative purposes only and do not constitute investment advice or an offer to provide investment advisory services. The tables and graphs contained therein are for informational purposes only and should not be taken into account when making any investment decisions. Past performance is not indicative of future results. The content speaks only from the date specified. Any projections, estimates, estimates, targets, expectations and/or opinions expressed in these materials are subject to change without notice and may differ from or contradict views expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives compensation from various organizations for advertising on affiliate podcasts, blogs and emails. The inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or Ritholtz Wealth Management or any of their employees. Investments in securities involve the risk of loss. For additional advertising disclaimers, see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see the descriptions Here.