During my corporate consulting days, I spent a lot of time analyzing the performance of active managers.

Many endowments, foundations, and retirement plans were trying to beat the market and exceed their own benchmarks.

Investment committees and boards of these nonprofits needed a way to track all their stocks, bonds, hedge funds, and private asset managers, so they often developed rating scales and watch lists.

Better performers would be given the green light. Middle class managers were given a yellow light. Underperforming managers are given a red light. Every three months the figures will be updated based on performance against benchmarks.

Sometimes a strategy like this can work by allowing you to invest in top performers and helping you release losers. However, this momentum play can only work for a certain period of time because outperformance in markets is temporary.

Even the best investors in the world underperform from time to time.

You will encounter a situation like this:

You hire a new manager who performs better because his returns look great, and he continues to underperform after you hire him. Of course, not everyone does this, but it happens more often than you think.

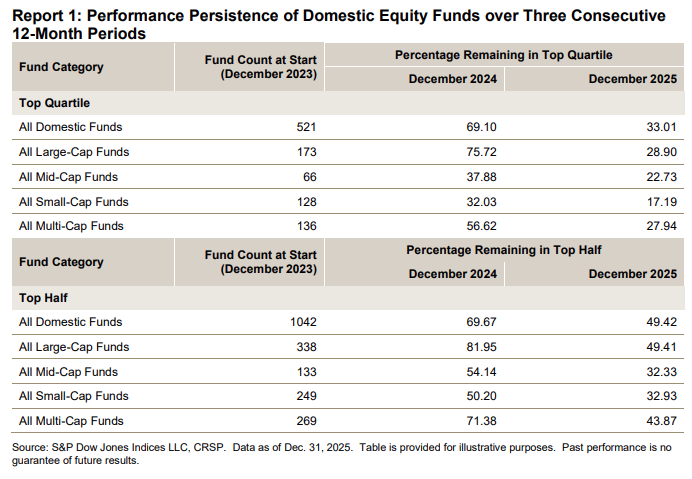

every year SPIVA publishes retention scorecard This looks at how often a manager’s superior performance in one period is followed by superior performance in the future.

The figures for US stock market funds for consecutive three-year periods are as follows:

In other words, 69% of the funds that were in the top quartile of 2023 returns remained in the top quartile in 2024. But in 2025, only 33% were still in the top quartile.

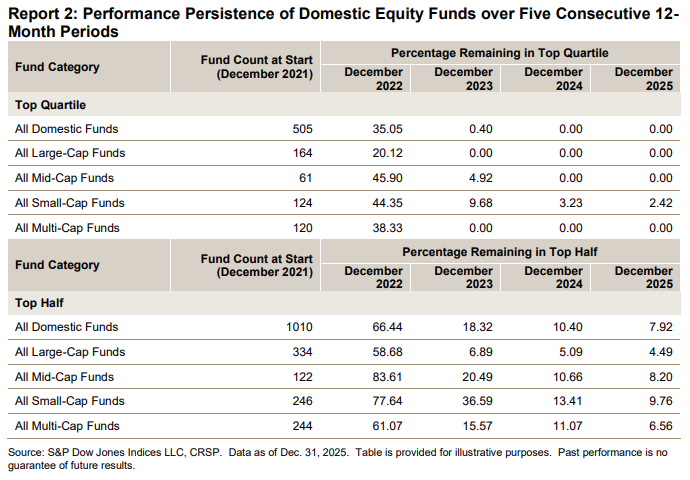

Now look at these figures over five years:

Starting in 2021, there were no funds remaining in the top quartile after 3, 4 and 5 years. Less than 10 percent of funds can stay in the top half of the top performers for five consecutive years.

So you need to get used to the fact that nothing and no one can consistently outperform the markets. This is what makes active management so difficult. It is difficult to collect stockBut choosing managers who will outperform the market can be even more difficult.

However, this is true for every strategy, whether active or passive.

I’ve been on a podcast tour for the last few months my new book. I’ve now received many questions about different ways to diversify a portfolio:

Is the 60/40 portfolio dead? Shouldn’t we update this with time?

How about adding gold to the portfolio? Or Bitcoin?

How about trend-following or managed futures?

How should investors consider diversifying their fixed income exposure given the bond bear market this decade?

How about buffer ETFs? Or option income funds?

What about private investments?

The good news is that there’s never been a better time to be an individual investor for the investment opportunities you can use for diversification.

The bad news is that the temptation to switch up your portfolio and overdo it by splitting your portfolio in half with too many funds and strategies has never been more appealing.

There is no right or wrong answer when it comes to diversification and asset allocation.

Some investors need to keep things extremely simple in a 3-fund portfolio. Some people prefer a single fund. When it’s anything more complex than that, they get overwhelmed.

Other investors choose to cover more bases from a diversification perspective and hold all kinds of different funds and strategies in their portfolios.

There is no perfect portfolio for every investor, but I have a rule of thumb that can help you understand whether the asset classes, strategies, and assets in your portfolio are right for you.

That’s what I call diversification test.

It goes like this: If the value of your investment drops, will you take the pain and buy more?

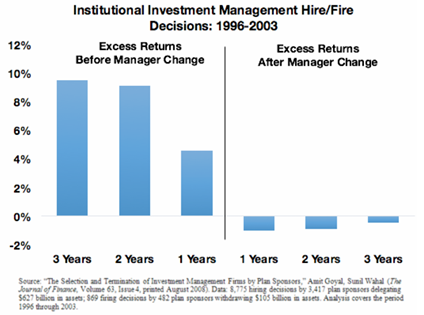

Many of the institutional investors I work with would do the exact opposite. Whenever a manager underperformed, they hit the eject button and fired him.

One reason for this is that most managers have more discretionary and complex strategies. Once you understand a strategy, it’s much easier to stick to it.

This is one of the reasons why I’m such a believer in rules-based strategies and index funds. With an on-demand manager, it’s hard to know whether you’re being disciplined for an overlooked process or simply oblivious to the fact that that process is no longer working.

I feel more confident in leaning into the pain when a rules-based strategy goes through a dry spell. Nothing is guaranteed in the markets, but if you know what you have and why you have it, you can set more reasonable expectations and have more confidence in your process. This way you won’t be tempted to constantly move in and out of different investments.

It’s easy to invest in something that’s going up.

The true test of any investment strategy or allocation is how you handle it when it lags.

Further Reading:

Creating the Perfect Portfolio