In a risk-free market, conviction is often the hallmark of long-term strength.

The current structure of Bitcoin (BTC) reflects this belief. Technically, BTC has recorded a quarterly loss in a row, with an average decline of around 20% each quarter. This is the first three-quarter losing streak since the 2022 bear market, leaving more than 50% of Bitcoin’s circulating supply underwater and putting long-term holders (LTHs) in tight focus.

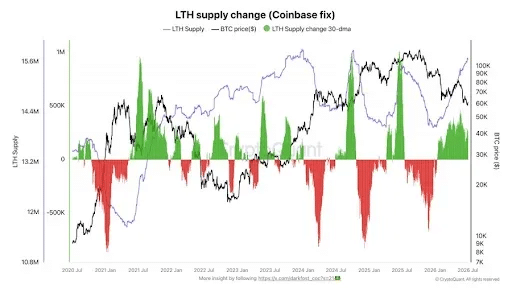

The logic is simple: LTHs now control 78% of Bitcoin’s circulating supply. In other words, the bulk of the underwater supply is held by investors who have held BTC for more than five months, covering the rise to the all-time high at $126,000 and the subsequent correction near $60,000. This makes their opinion a key factor in shaping Bitcoin’s Q3 and Q4 outlook.

What is particularly notable is that long-term investors do not sell on weakness.

Instead they suck it up. Despite the correction, LTH supply hit a record high in June, reinforcing the view that investors are continuing to accumulate rather than exit. Historically, Bitcoin has tended to bottom out when long-term holders begin to capitulate. So far this cycle is developing differently.

However, long-term investors remain highly sensitive to macroeconomic developments as they tend to price in the broader economic outlook when positioning their portfolios. From this perspective, of Bitcoin The surrender phase may not be over yet.

Why Bitcoin’s strongest group may soon face its toughest test

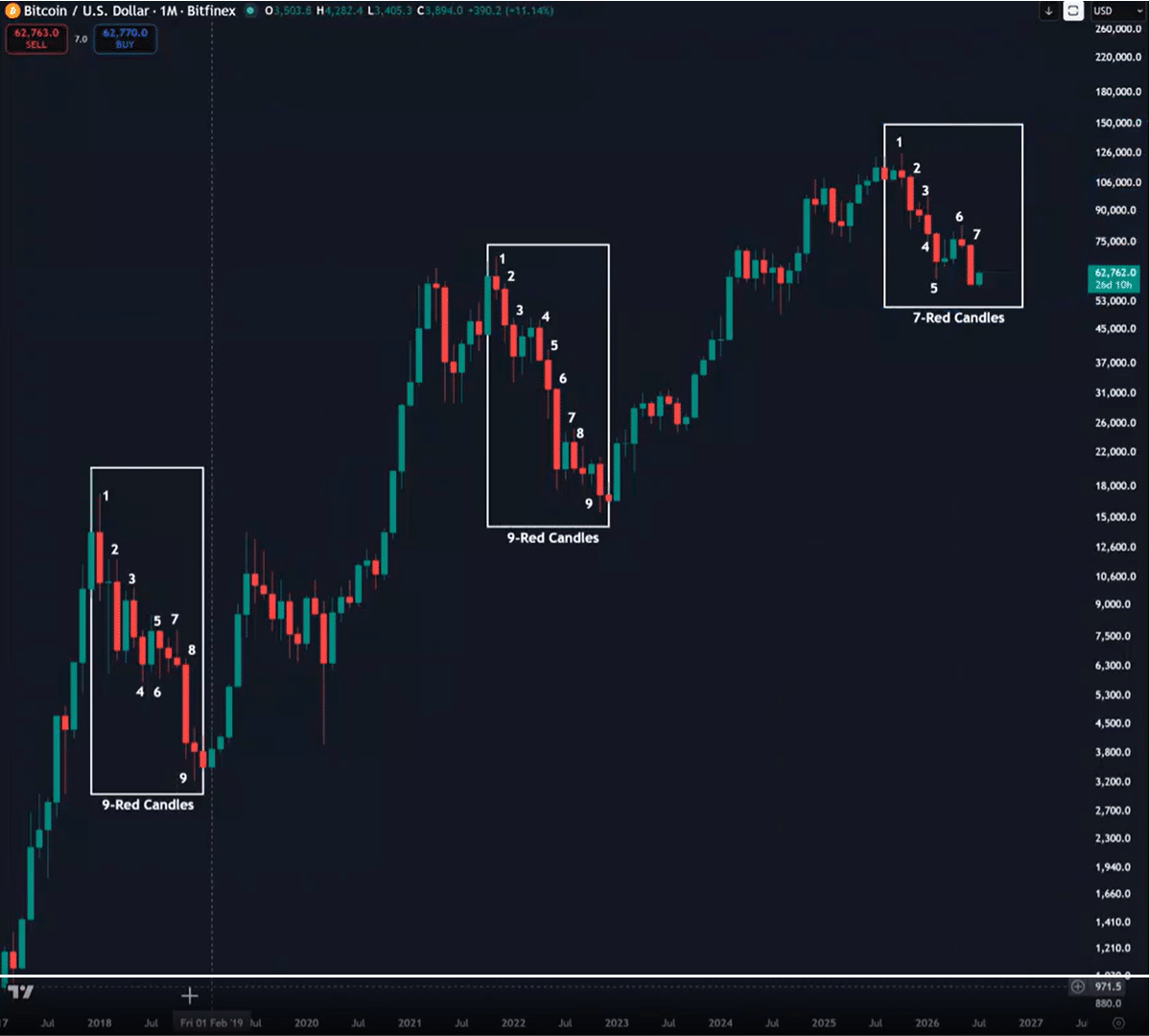

Bitcoin’s past bear markets provide a useful reference point for the current cycle.

However, before drawing parallels, it is useful to look at what has changed. macro- front. Interest rate expectations for the Fed’s July and September FOMC meetings have changed significantly. While the probability of the Fed not changing interest rates in July is 77%, the probability of a 25 basis point increase is 23%.

By September the picture becomes more balanced. Markets are pricing in a 41% probability of no change, a 47% probability of a 25 basis point increase, and a 10.5% probability of a 50 basis point increase. In other words, markets are increasingly betting for tighter financial conditions in the fall, rather than the rate cuts many expected.

This shift makes Bitcoin’s previous bear markets a relevant reference point.

As the chart above shows, both the 2018 and 2022 bear cycles did not reach a bottom until BTC printed nine consecutive monthly red candles. The current cycle has produced seven so far. If the historical pattern holds, there may still be enough room for Bitcoin’s capitulation phase to advance before a durable base forms.

This is where the expanding pool of underwater long-term owners meets the increasingly uncertain macro backdrop. If this cycle follows the same scenario, long-term holder capitulation could signal Bitcoin’s latest fiasco, potentially sending BTC towards the $50,000 region by the end of Q3 before a bottom forms.