My first real job was at a small, independent consulting firm.

In fact, the company was so small that we had no employee retirement plan. Back then, it was harder for a small business to have a 401k plan than it is today.

That’s why I decided to buy mutual funds from Vanguard. The only problem was, at the time, the minimum amount required to purchase an index fund was $3,000. I didn’t have $3,000 because I wasn’t making very much money and I needed more time to save that much money after graduating from college.

I had to wait a long time to open an account and invest in the stock market.

I read it in 2006 or so. What Works on Wall Street? By Jim O’Shaughnessy. It was my first real foray into factor investing. Jim effectively demonstrated the need for a quantitative investment framework using a variety of value, quality and momentum factors. I liked the ideas in the book, but when I did the math on how much it would cost to buy 50 stocks with a commission of $19.99 per trade, it was too costly for my meager portfolio.

Barriers to market entry were much higher back then. Today, these obstacles have been virtually eliminated.

Minimums effectively no longer exist. You can buy fractional shares. There are ETFs where you pay some basis points to diversify a basket of stocks in almost any combination you can think of. There are target date funds. No more commissions. You can open an investment account (brokerage or IRA) in minutes from your smartphone. You can connect your bank account, deposit money into your account and invest immediately.

You no longer have to go to a brick-and-mortar building, fill out a bunch of paperwork to open an account, write a check to fund the money, and wait days to finally invest.

You don’t need to save months and months to meet high minimums while you’re out of the market. You no longer need to pay sky-high commissions or front-end loads to buy shares in stocks or funds.

You can automate your contributions, buy/sell decisions, dividend reinvestment, rebalancing, and more.

What are the consequences of this lowering of barriers to entry?

For one thing, more people are investing in the stock market.

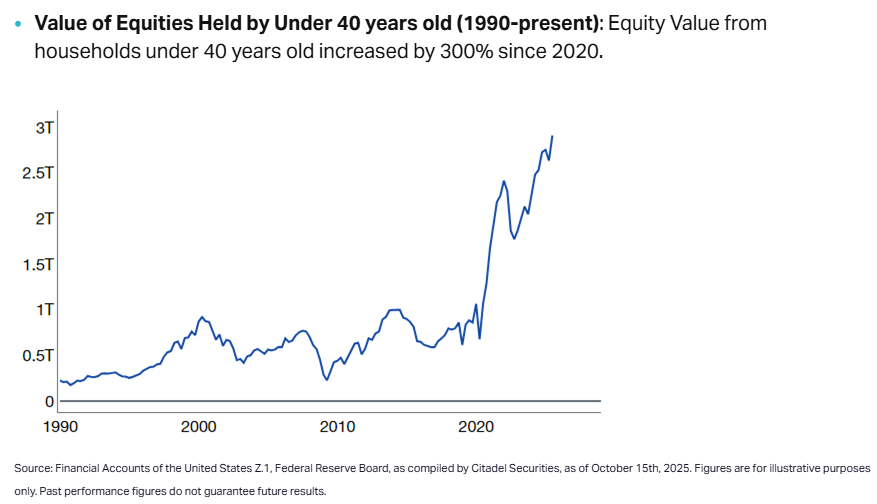

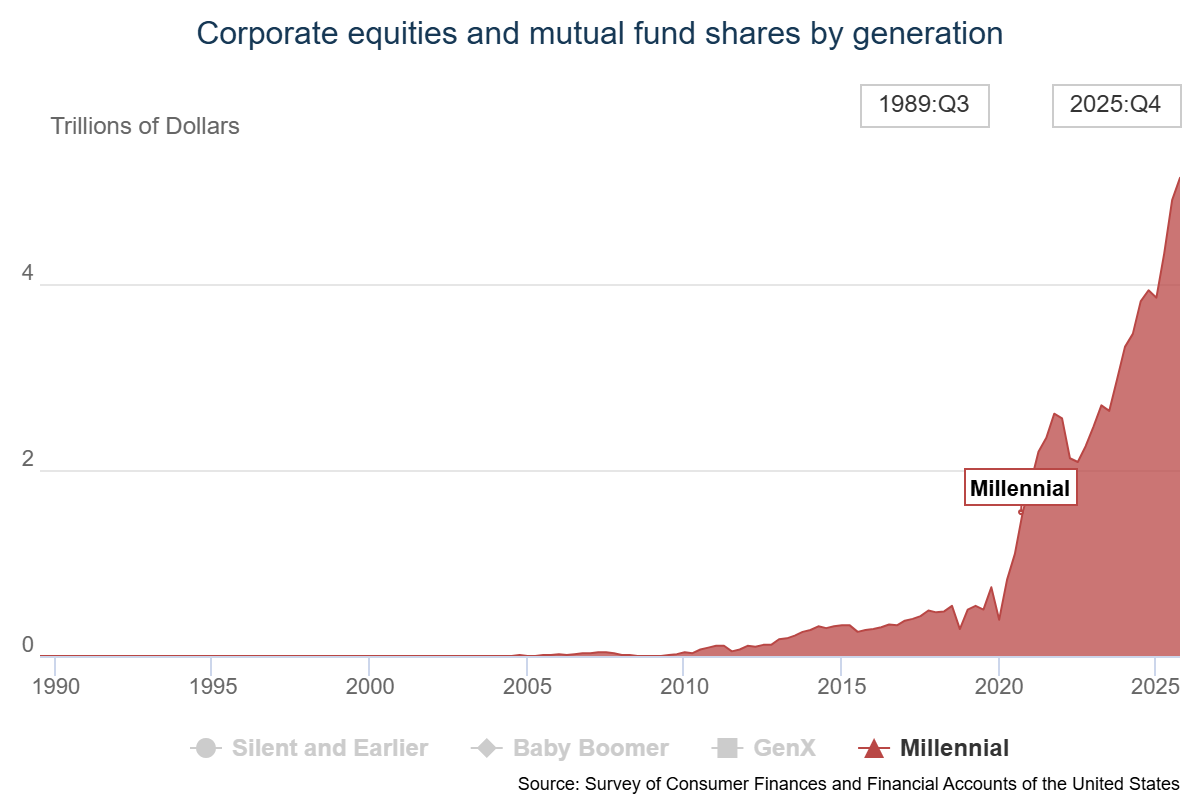

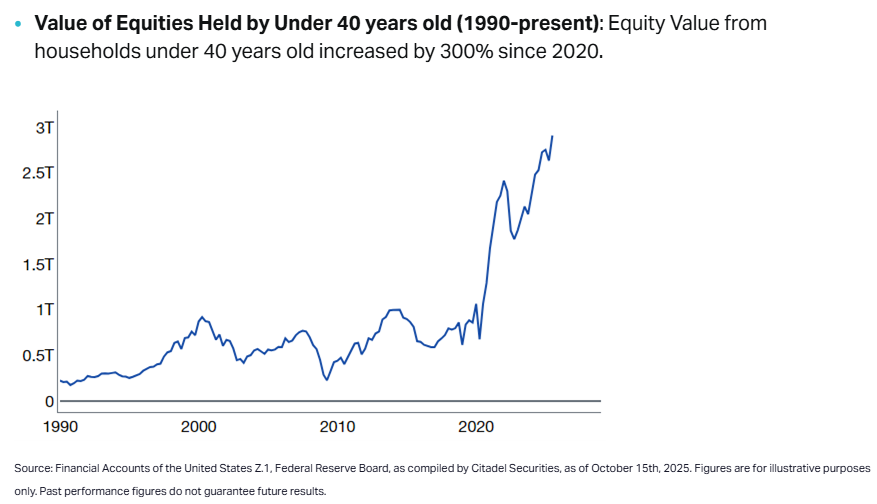

More young people are investing in stocks:

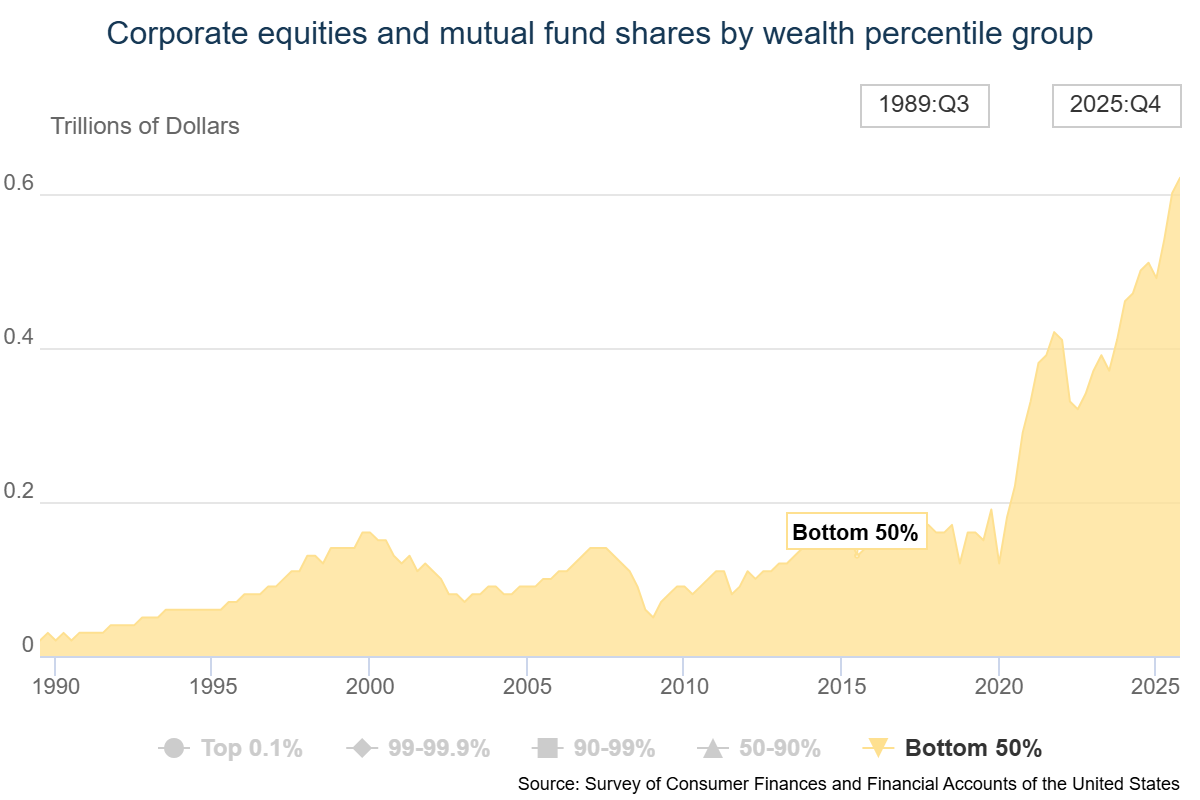

More people in the bottom 50% invest in stocks:

There are other reasons why these charts are rising, but making it cheaper and easier for people to invest certainly helps.

Automated investment revolution This is probably one of the reasons why valuations have moved higher over time.1 Before the advent of 401k plans, IRAs, online brokerages, and automated investing technology, far fewer households were investing in the stock market.

Having a large group of people buying regularly, regardless of fundamentals, should have an impact on valuations.

Lack of friction can also have its disadvantages. It has never been easier to move in and out of investments by over-trading your accounts.

The trading volume of SPY, the oldest ETF on the market (in the USA), is in the range of 80-100 million per day. This is something like 8-10% of the fund turned over each trading day, so the average holding period for this fund is maybe a few weeks.

Low barriers to entry can turn a passive product into an active strategy very quickly.

I’ve been thinking about barriers to entry in light of the AI boom.

Artificial intelligence should make it easier for you to learn anything you want. Companies are spending trillions of dollars to make it easier for us to ask supercomputer models how things work. With nearly instantaneous research, analysis and feedback, you can learn about any topic imaginable and ask as many follow-up questions as you want.

Barriers to entry into learning have been leveled.

With the caveat that no one knows how AI will turn out, here are some potential pitfalls and benefits of this new world:

Skill atrophy. Some people will outsource their thoughts and become even stupider. Students will cheat. Articles, notes and reports will be written entirely by artificial intelligence.

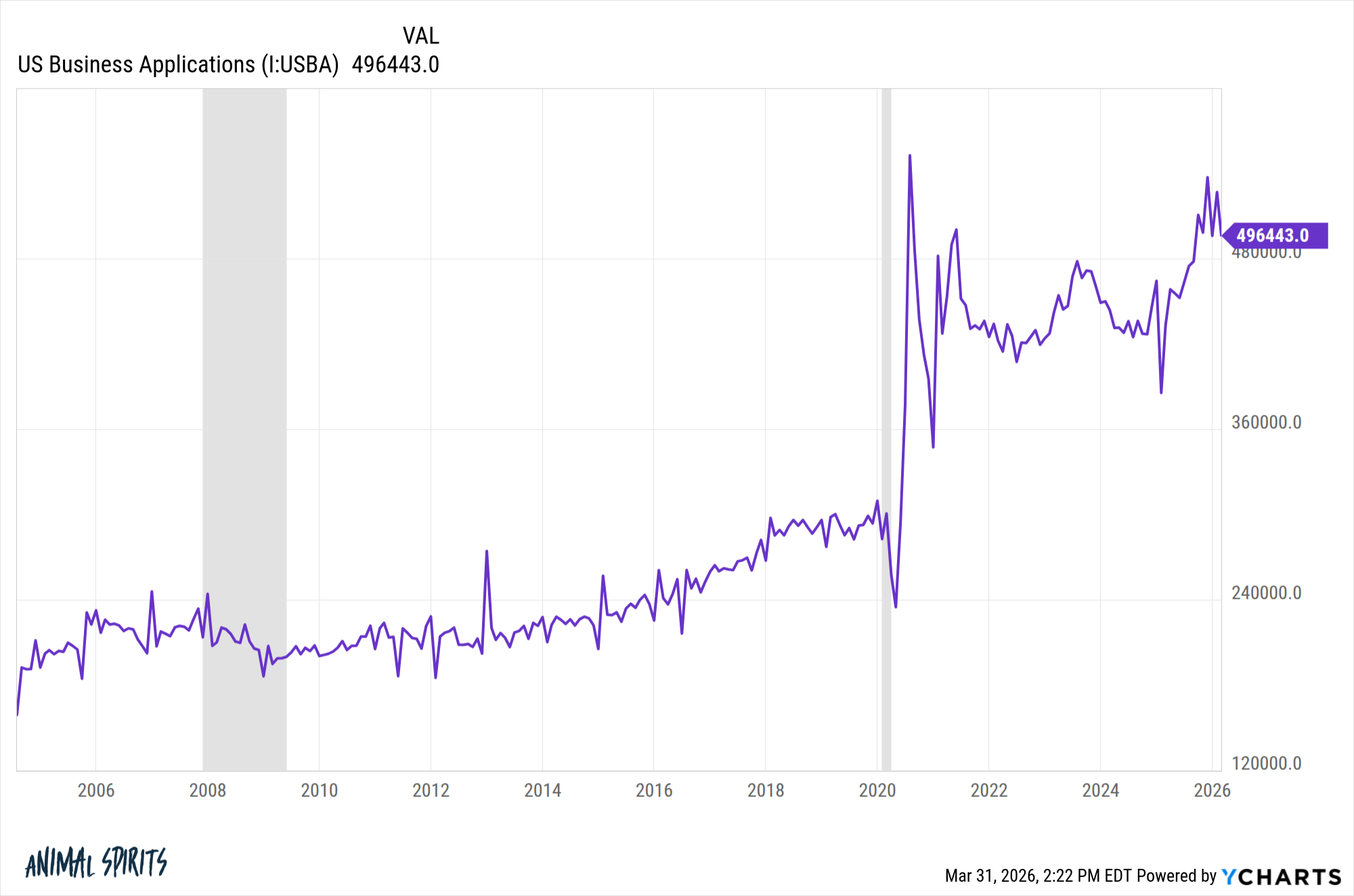

Job formation will explode. One of the unintended consequences of the pandemic was the explosion of new business applications:

I think AI’s lowering of barriers to coding, learning, and entry into certain tasks will make it easier than ever to start your own business.

People who are not interested in technology will now be able to compete in more advanced technology fields.

AI bias. Some people trust anything and everything AI tells them. These Masters are not always accurate. You need to check their work.

Personalized teachers. In theory, AI should allow for a personalized teacher/educator for each child with access to these tools. This is what I want for my children because they all have different strengths, weaknesses, and learning styles.

Closing the skills gap. People who don’t pursue higher education can potentially level up and save a lot of money in the process.

The Jevons Paradox will come into play. If artificial intelligence does the work of 5 paralegals, do you think lawyers will work more or less? If billable hours are still the business model, everyone is getting sued.

Some medical professionals will likely see an increase in referrals as AI makes it easier to screen patients with specific problems or needs.

I use Claude more to help with market research. This saves me time on some projects, but it all makes me more productive so I can focus on other tasks. It allows me to get more work done.

There will be other unintended consequences. I don’t know what they are yet.

Further Reading:

Pros and Cons of Artificial Intelligence

1Coupled with the fact that technology has made companies much more efficient and technology companies now dominate the markets.