A reader asks:

I’m in my mid-30s and I’m chasing FIRE. If all goes well, my wife and I should reach our goal number by the time we turn 40. I’m not a big fan of bonds, and instead want to keep a larger cash position equivalent to about two years’ worth of expenses in a high-yield savings account and maintain a more aggressive mix of U.S. and international ETFs. My question is: Does it make sense to do this? Am I leaving money on the table by using only cash/savings and avoiding bonds or other low-risk alternatives?

I’ve been getting a lot of questions lately about the desire to become financially independent and retire early. Many people really want to retire at a relatively young age. We can talk about the ATEŞ movement another time.

This is an asset allocation question. I enjoy the in-depth look at asset allocation.

Let’s do this.

This person is asking about your weightlifting portfolio.

On one side of the barbell you have risky assets (stocks) and on the other side you have risk-free assets (cash).1

Since both are technically fixed-income assets, bonds are closer to cash than stocks on the risk spectrum, but some consider them to be in the middle of the bar in this analogy.

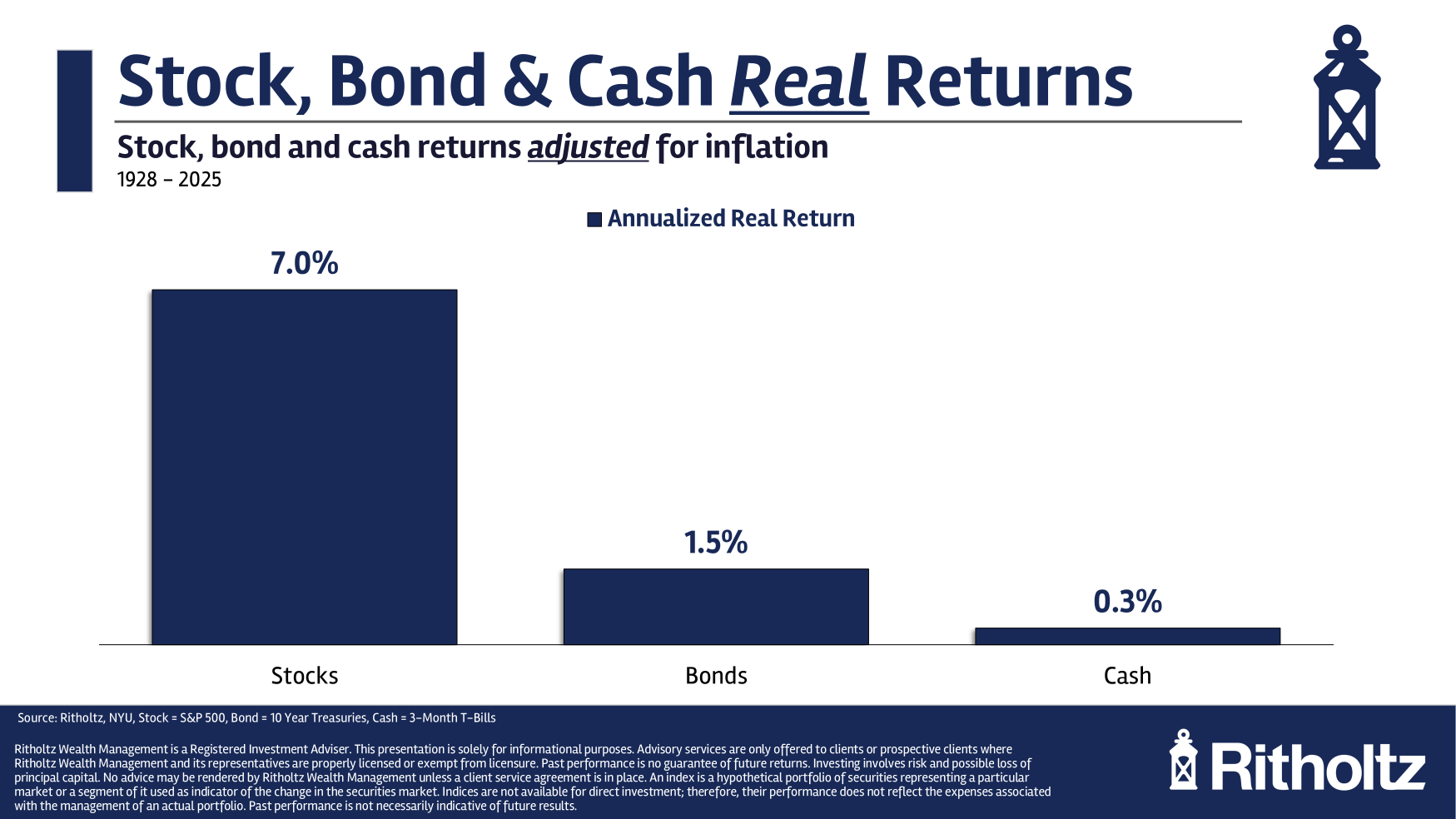

Here are the historical annual returns for each of these three major asset classes:

Over the long term, cash yields have remained relatively close to bond yields.

Of course, the biggest risk for any fixed income investor is inflation. Here are the inflation-adjusted real returns:

The good news is that the cash position has kept pace with inflation over time. The bad news is that you wouldn’t make much more than the inflation rate.

There are many investors who no longer want to hold bonds in their portfolios. You don’t need to look for too many answers on this subject.

See returns in 2022:

- S&P 500 -18.0%

- 10-year Treasury bonds -17.8%

- 3 month treasury bill +2.1%

Rapidly rising interest rates combined with rapidly rising inflation can be a bad combination for government bonds. But short-term treasuries have done very well, thank you very much. You don’t have to worry about interest rate risk when it comes to a cash-like position.

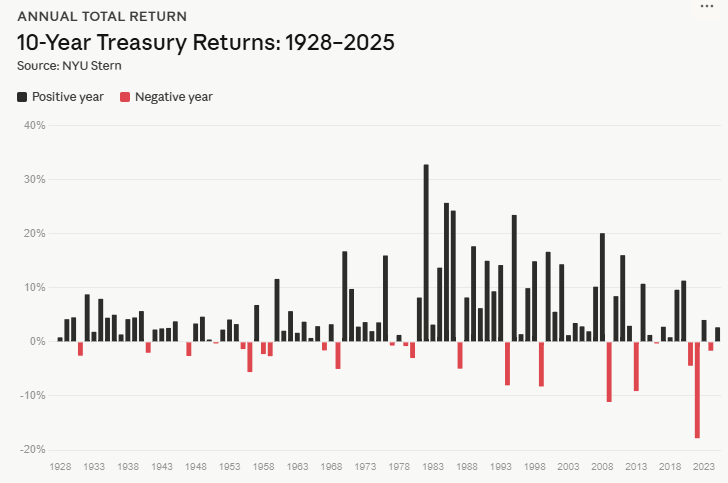

Let’s look at the annual return differences between bonds and cash to see why this is the case.

First bonds:

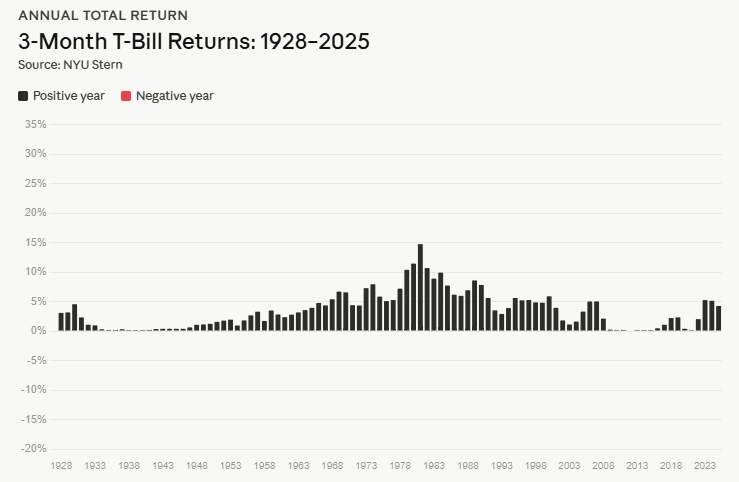

Now treasury bills:

There’s a reason I use the same scale in these charts. Bond yields can be much higher than cash yields, but there have been a fair number of down years for Treasuries. I’m counting back 19 years for the bonds, which means the win rate is around 80%.

There were no gap years for cash.

That’s why many investors are approaching the idea of allocating cash in a dumbbell-like portfolio.

Treasury bills are one form of cash investment, but it can also be a high-yield savings account, money market, or CDs.

So far we have looked at very long term data here. It is also useful to think about risk in terms of shorter time frames. Some environments are better for bonds, others are better for cash.

This cycle has been much better from a cash perspective.

Here are the annual returns for each from 2022 through 2025:

It was quite possible The worst decade ever for bonds.

But recency bias aside, it wasn’t that long ago that cash was trash. The Fed kept interest rates steady throughout much of the post-GFC period. In fact, from 2008 to 2021, the average 3-month treasury bill yield was just 0.55%.

Guess what the annual return was at that time? About 0.5% per year. Over the same time period, the 10-year Treasury rose at about 4% per year.

There have been periods in the past when returns have varied significantly.

The combination of the Great Depression and World War II led to a prolonged period of financial repression with very low short-term interest rates from 1932 to 1954:

Cash bonds underperformed by a wide margin and also lost money to inflation (2.7% annually).

During the inflationary period from 1966 to 1981, cash was king:

While bonds have been smoked by rising interest rates and high inflation, cash has outperformed. Short-term rates adjust faster so you don’t have to worry about rates rising with a cash-like position.

I could keep making such comparisons. The point is that the economy is cyclical, so the performance of fixed income assets will also be cyclical.

The biggest risk for bonds will be if interest rates rise rapidly. The biggest risk to cash will be if the Fed keeps short-term interest rates low for an extended period of time. The biggest risk to both bonds and cash will be high inflation.

Keeping your spending reserves in cash makes sense from a liquidity perspective. You don’t have to worry about your face value decreasing.

But there are other risks to consider.

It really depends on how much emphasis you place on yield, inflation protection, and deflation protection.

I covered this question in more detail in a brand new episode of Compound Ask:

Bill Sweet He joined us to discuss questions about reducing equity risk in retirement, hitting your retirement number, taking care of your parents financially, convincing yourself to sell stocks, and some advice for a young investor.

Further Reading:

4-Year Rule for Retirement Expenditures

1I have never used the term ‘risk-free’ very comfortably because every investment involves some form of risk. This is financial jargon. I need to get over this.