According to a recent report from Dune, a significant portion of the liquidity that users provide to decentralized exchanges is not actually used to speed up transactions.

To put things in perspective, concentrated liquidity was created to improve the capital efficiency of decentralized exchanges. This was done by allowing liquidity providers (LPs) to distribute funds within specific price ranges where trading was more likely to occur.

However, the study found that average liquidity of 29.4% in the first half of 2026 was outside the active trading range. Likewise, no transaction fees were charged.

This amounted to approximately $542 million per week in idle capital and an estimated $150 million in lost annual fee revenue for liquidity providers across the four protocols.

For context, the 4 protocols included are Uniswap v3, Uniswap v4, PancakeSwap v3, and Aerodrome Slipstream.

Underutilized concentrated liquidity

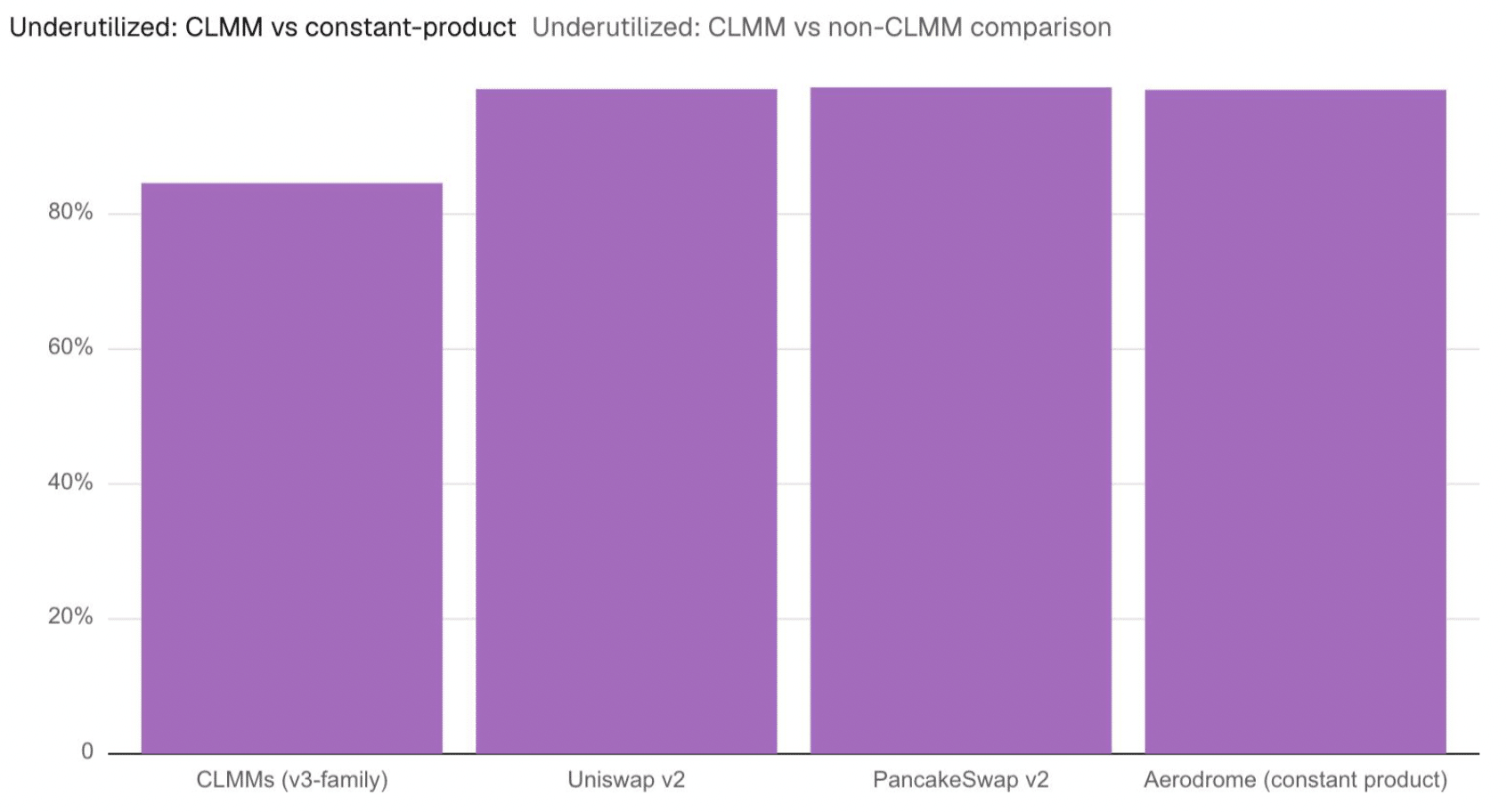

Considering the liquidity that is technically available but never used, it appears that approximately 85% of capital is underutilized.

The fact that more than $200 million of idle liquidity has not been repositioned for more than 90 days may be evidence that many LPs are not actively managing their assets.

This also showed that although concentrated liquidity should improve efficiency, it is still difficult for many LPs to hedge their positions in line with market prices.

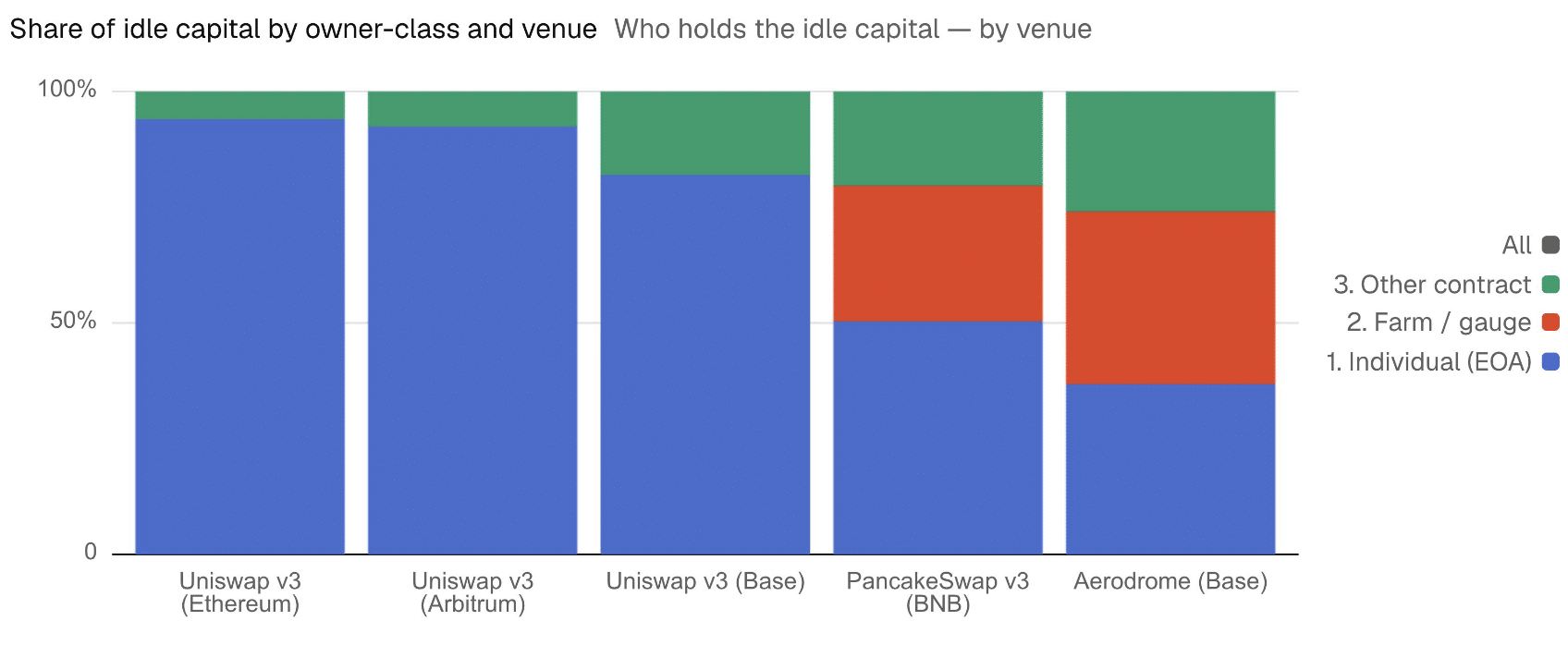

Individual investors suffered the most

Additionally, the study found that automated managers maintain capital activities, while individual investors hold the majority of idle liquidity.

wallets open Ethereumfor example, it owned 94% of idle capital and 91% of capital. Uniswap v3 liquidity. At Arbitrum, 92% of idle liquidity and 78% of liquidity were under control. At Base, individual users managed 82% of idle capital, even though smart contracts held approximately 50% of the liquidity.

This was because only 6.5% of their positions were out of range, compared to around 30% in wallets. This also showed that automated managers were much better at preserving liquidity than individual LPs.

additional spaces

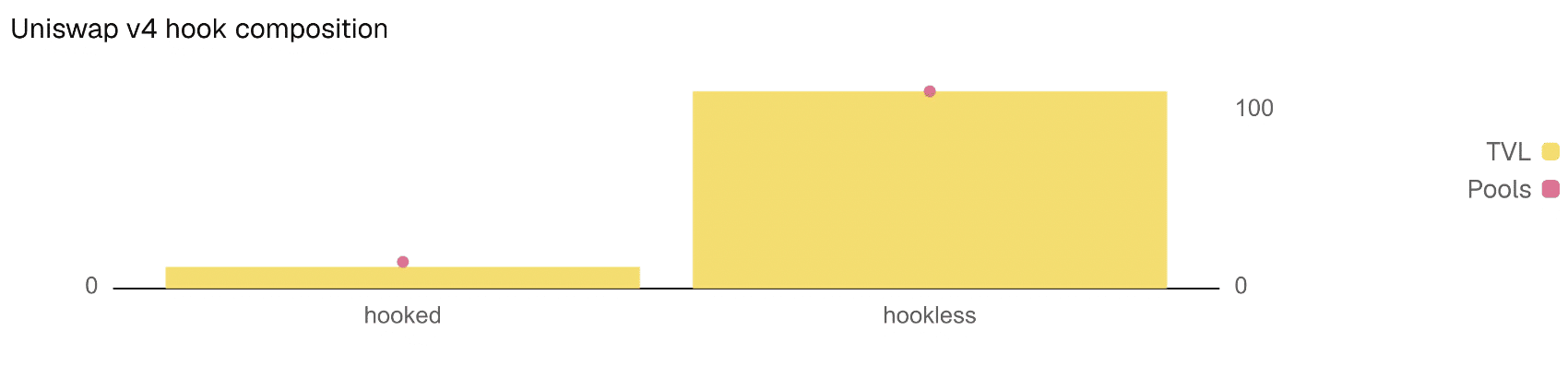

Finally, the study found that the idle liquidity issue was not resolved by Uniswap v4.

Like Uniswap v3, around 30.5% of its liquidity is still out of range even after adding hooks that could allow idle capital to be used in external return strategies.

Additionally, only 10% of v4’s TVL actually uses hooks, and none of them are currently generating returns from idle liquidity.

Final Summary

- In the first half of 2026, approx. 29.5% of liquidity was outside the active trading range.

- Instead of AMMs, the majority of idle liquidity belonged to individual investors.