Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Here is an email I received recently:

I’ve been doing some experiments by taking the questions you and other online financial people have answered and asking various AIs. Their answers are very good, more comprehensive, and often better than the answers human “experts” provide for the same questions.

Not only that, but I can instantly import every financial document, my personal information, my feelings about risk or market downturns, and any other thoughts I have for the AI to craft an investment plan exactly for me. Then I can ask questions about anything (most of which I would be embarrassed to ask a professional). And I can have it adjusted and recalibrated instantly, whenever I want! He seems to have expertise in every area – retirement withdrawal, tax implications, inheritance, etc. The teacher even gave me information about my retirement that I had not known or considered before.

I know you’ll say people want “face-to-face” human interaction, but financial advice seems like perfect prey for AI to take over almost instantly.

When you put it that way, it looks bleak for financial advisors.

I agree that AI will make things easier for many people who have questions and don’t know where else to look for answers. Tools for do-it-yourself investors have never been better, and AI will continue this trend.

Some may think I’m biased because I work in wealth management, but I strongly disagree that this means the end of financial advisors.

The world of advice will be better for both DIYers and financial advice clients.

Let me explain.

I know a consultant who started this business in the 1980s and 1990s. Back then, the business was basically raising investment funds on behalf of your clients. This is it.

If all you did was select funds on behalf of your client, you would never be able to compete as a financial advisor today. Robot advisors do this at a fraction of the cost and are much more efficient in this regard.

So why haven’t robo-advisors put financial advisors out of business?1

Trust is a big part of this. People enjoy working with other people. Finance is a service-based business that sells both. concrete and intangible assets.

Some people are willing to ask the AI all the questions, upload all the statements, create a plan, and then execute that plan themselves. But this requires a lot of work and others prefer to outsource and move on with their lives.

It’s also important for some people to have a team in their corner. What happens if there is a problem with the IRS? Or did you lose your money while moving from one financial institution to another? Some people need to take responsibility.

You can make the most customized exercise plan you want right now. Some people still prefer to use a personal trainer. Information is useless if you don’t take action.

Customers will also expect more tools and services in the future.

Goals-based financial planning came in the wake of mutual fund diversions. This is a big part of the process, but it’s also true that advisory clients rightly expect much more from goal setting and portfolio management.

Since I joined Ritholz returned in 2015We added tax practice, insurance services, estate planning (including in-house counsel), a family office division, corporate retirement planning, and corporate investment management. We also continue to add new tax-sensitive investment platforms that assist with the financial planning process.

Technology played a role in this growth, but it also meant many more people. More customer service representatives, more merchants, more advisors, etc. Because you need someone to explain how this all works. Someone needs to interact with systems to make them work with other systems.

In fact, one of our biggest challenges now is to manage more people. We had fewer than 10 employees when I joined, now we have almost 90 employees.

Will artificial intelligence make our applications more efficient in the future? Definitely. In some ways it already is, and over time we will definitely implement more AI-based productivity tools. But artificial intelligence will not solve people’s problems, and people’s problems are endless.

Some think AI will allow advisors to serve more clients, which could lead to some consolidation in the space. This is possible for type A advisors. But many in the industry will become better advisors to the clients they already serve.

And if your work becomes more productive, you can spend more time with your family or relax a bit.

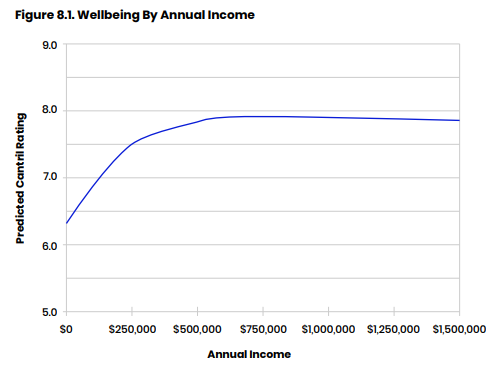

A. Kitces Report Research on advisor wealth has found that more money increases wealth, but this remains constant:

A higher client load and more money may not be as attractive as more free time.

It doesn’t have to be a zero-sum game with winners and losers.

DIY investors who would likely never use a financial advisor will now have more personalized advice and a better platform to ask questions.

Consulting clients will have more tools, more services, improved reporting software and a better customer experience.

Consultants will also be able to better serve their client base while also becoming more efficient in the process.

It’s a win-win-win situation.

I was in Miami this week for Future Proof Citywide and all the talk at the event was about AI in asset management. The first night in town we had a big dinner with a bunch of people from the industry and I asked. Michael Kitces For his thoughts on AI potentially replacing financial advisors.

He had very strong ideas backed by data.

That’s why Michael and I asked him to come on our Animal Spirits livestream and share his thoughts on the subject:

we had too Phil Huber We appear on the show to talk about what’s going on with the special loan from Cliffwater and the bonus Animal Spirits fries at the end of the show.

Subscribe Compound so you won’t miss any episode.

Further Reading:

My 10 Years at Ritholtz Asset Management

Now here’s what I’ve been reading lately:

Books:

1Read Josh’s article on robo advisors vs human advisors Here.