There are some concepts in life that make sense the moment you hear and learn them.

Occam’s Razor. 80/20 rule. Murphy’s Law. Index funds.

Indexing immediately made sense to me. Low costs. Tax efficient. Low turnover. Low maintenance. Simple. And this is very difficult to overcome in the long run (even by professional money managers).

I’ve been investing in index funds for over 20 years. Anything valid for indexing is only obtained if stronger during this time.

My basic expectation was always that index funds would outperform 70-75% of actively managed funds.

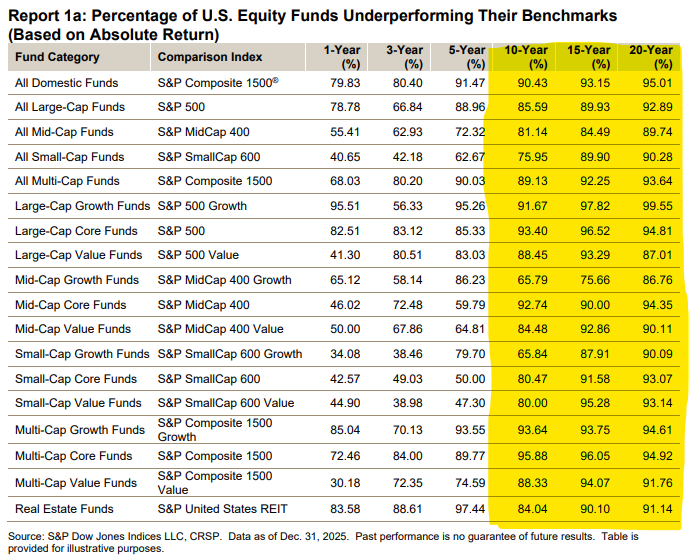

SPIVA Scorecard Recent years have shown this rate to be 90% or more for a wide range of stock market styles over 10, 15 and 20 year time frames:

One of the reasons I like index funds is that they are difficult to pick stocks. Indexing allows you to cast a wide enough net to make sure you keep the big winners, which more than offsets the big losers.

I didn’t fully understand how intense the winners’ returns were until I read Hendrik Bessembinder’s work. In 2018 Bessembinder published: Are Stocks Outperforming Treasury Bills?

His research found that over the long term:

- Almost 60 percent of stocks underperform Treasuries.

- Most other stocks only marginally outperform cash.

- About 4% of stocks account for the vast majority of overall gains.

This research was like confirmation bias on steroids for indexers. I knew the stock market was concentrated but I didn’t realize it was This concentrated. This is a big deal for index funds because you automatically own the biggest winners. And these gains tend to be huge.

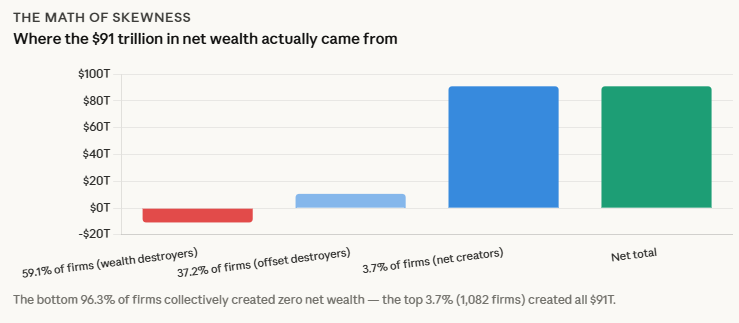

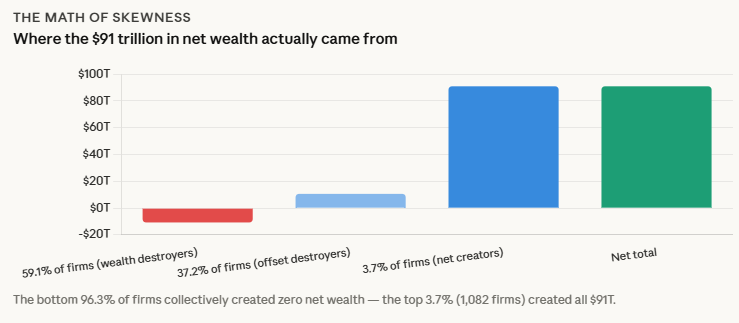

Bessembinder published an update on his findings last week in a new paper titled . One Hundred Years in the US Stock Exchange. Over the past decade, the stock market’s long-term gains have become more concentrated:

During the 1926-2016 period studied in Bessembinder (2018), 89 firms accounted for half of the $43 trillion in net wealth creation. When the results of the last nine years are included, just 46 companies account for half of the $91 trillion in net wealth created over the entire century.

My new research assistant, Claude, scanned the data from his research to show it more visually.

Let’s take a better look at how markets are trending towards big winners:

It’s almost hard to understand how much money is being created by such a small subset of companies.

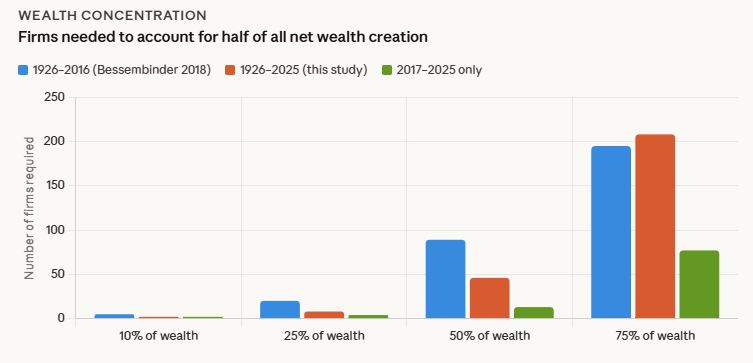

Another thing to look at is this based on the percentage of wealth created using the original study and updated figures:

Between 1926 and 2025, just 208 companies created 75% of the wealth in the stock market.

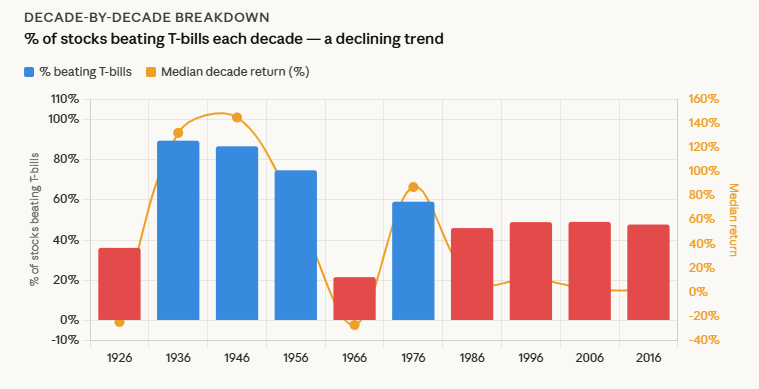

Here’s a breakdown of how many stocks are outpacing Treasuries by 10-year gains:

The win rate over the past 40 years has remained surprisingly steady at around 50%; This means that half of the companies are beating cash, while the other half are not keeping up with the risk-free rate.

Of course, this study A lot long term. Individual stocks can still post gains before eventually falling. Not every investor is a buy-and-hold type. There are other opportunities in between.

And index funds are nothing special. There are other ways to create tax-efficient, long-term investment strategies within a simple, rules-based framework.

I’m not saying indexing is the only way to invest.

But the data shows why index funds are so hard to beat over the long term.

Michael and I discuss Bessembinder’s research, history’s best stocks, and much more in this week’s Animal Spirits video:

Subscribe Compound so you won’t miss any episode.

Further Reading:

We debunk the stupid myth “It is a passive bubble”

Now here’s what I’ve been reading lately:

Books:

This content containing security-related opinions and/or information is for informational purposes only and should in no way be relied upon as professional advice or endorsement of any practice, product or service. No guarantee or warranty can be given that the views expressed herein will apply to any particular case or circumstance and should not be relied upon in any way. You should consult your own advisors on legal, business, tax and other related matters regarding any investment.

The comments contained in this “post” (including any associated blogs, podcasts, videos, and social media) reflect the personal opinions, perspectives, and analyzes of Ritholtz Wealth Management employees making such comments and should not be considered the opinions of Ritholtz Wealth Management LLC. or its respective affiliates or a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any security or digital asset or performance data are for illustrative purposes only and do not constitute investment advice or an offer to provide investment advisory services. The tables and graphs contained therein are for informational purposes only and should not be taken into account when making any investment decisions. Past performance is not indicative of future results. The content speaks only from the date specified. Any projections, estimates, estimates, targets, expectations and/or opinions expressed in these materials are subject to change without notice and may differ from or contradict views expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives compensation from various organizations for advertising on affiliate podcasts, blogs and emails. The inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or Ritholtz Wealth Management or any of their employees. Investments in securities involve the risk of loss. For additional advertising disclaimers, see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see the descriptions Here.