Charlie Munger once said there are three ways a smart person can go bankrupt: drink, women, and leverage.

It seems like many investors are using leverage theory for a test run.

The South Korean stock market is on fire, up almost 200% in the last 12 months alone.

Investors there realized this and leveraged:

According to the Korean Financial Investment Association’s statement on Wednesday, the outstanding balance of margin loans stood at 36.3967 trillion won as of the previous day. This figure represents an increase of approximately 33%, from 27.4207 trillion won at the beginning of the year to 8.976 trillion won. The loan balance secured by invested securities, which investors who have already exceeded their credit limits use stocks and bonds as collateral, also increased by nearly 2 trillion won this year, reaching 25.9297 trillion won. Despite the burden of collateral requirements, investors are pursuing additional purchases through dollar-cost averaging.

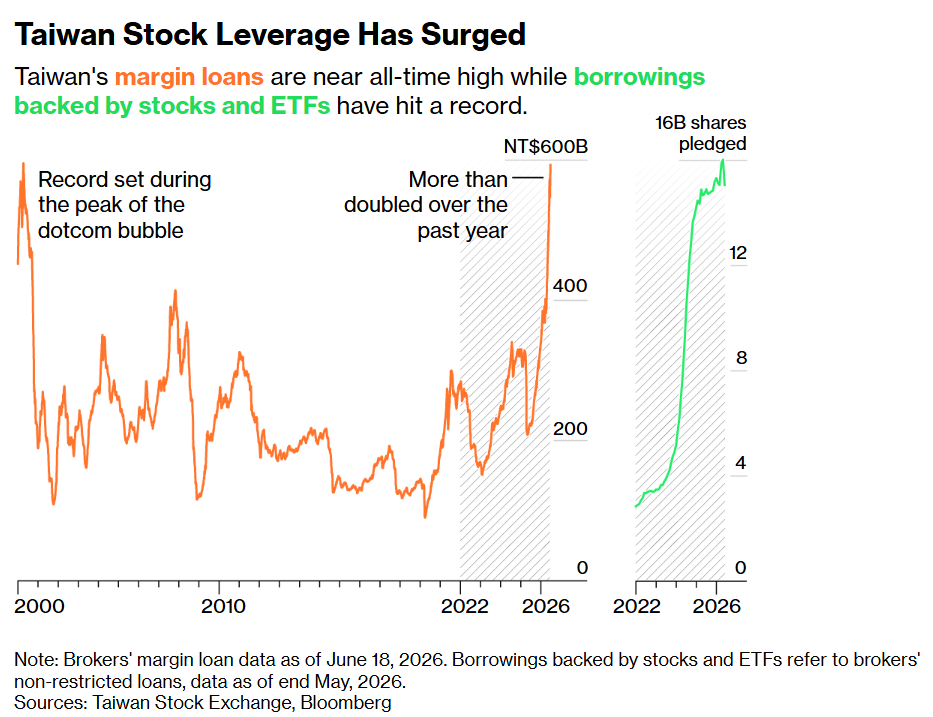

The Taiwanese market has also caught the AI disease. The market has doubled in the past year.

Investors borrow money like the drunken sailors there:

Andy Cheng is 26 years old, unemployed, and, with the help of some borrowed money, the proud owner of $60,000 worth of Taiwanese tech stocks. And in many ways, he speaks for the entire island of 23 million people when he dispenses this advice: “Buy any stock and you’ll make money.”

Up, up and away:

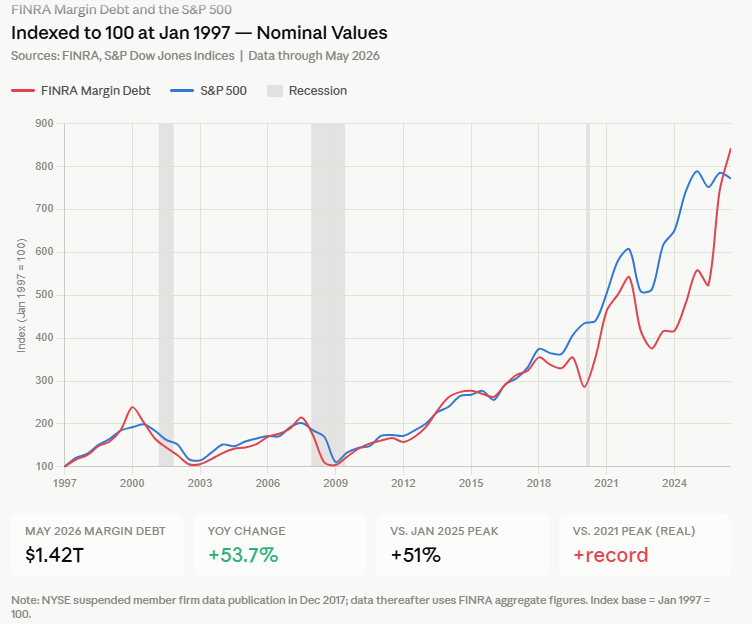

Americans never like to be left out of a boom, so borrowing from the stock market is done here too. Where is this from Wall StreetJournal:

U.S. margin debt, or what investors borrow from brokerages to buy securities, rose 54% in May from a year earlier to a record $1.4 trillion, according to Finra data. Meanwhile, high-risk leveraged exchange-traded funds and their related options trading are booming, doubling or tripling the daily movement of underlying stocks.

This number does not include things like leveraged ETFs. box spread credits or embedded leverage in instruments such as futures and options.

So it’s probably much higher than that.1

My take on leverage in the stock market is that I deal with it on a micro level rather than a macro level. I don’t think leverage will crash the entire stock market, but it could certainly blow up some of the names and investors with the biggest momentum.

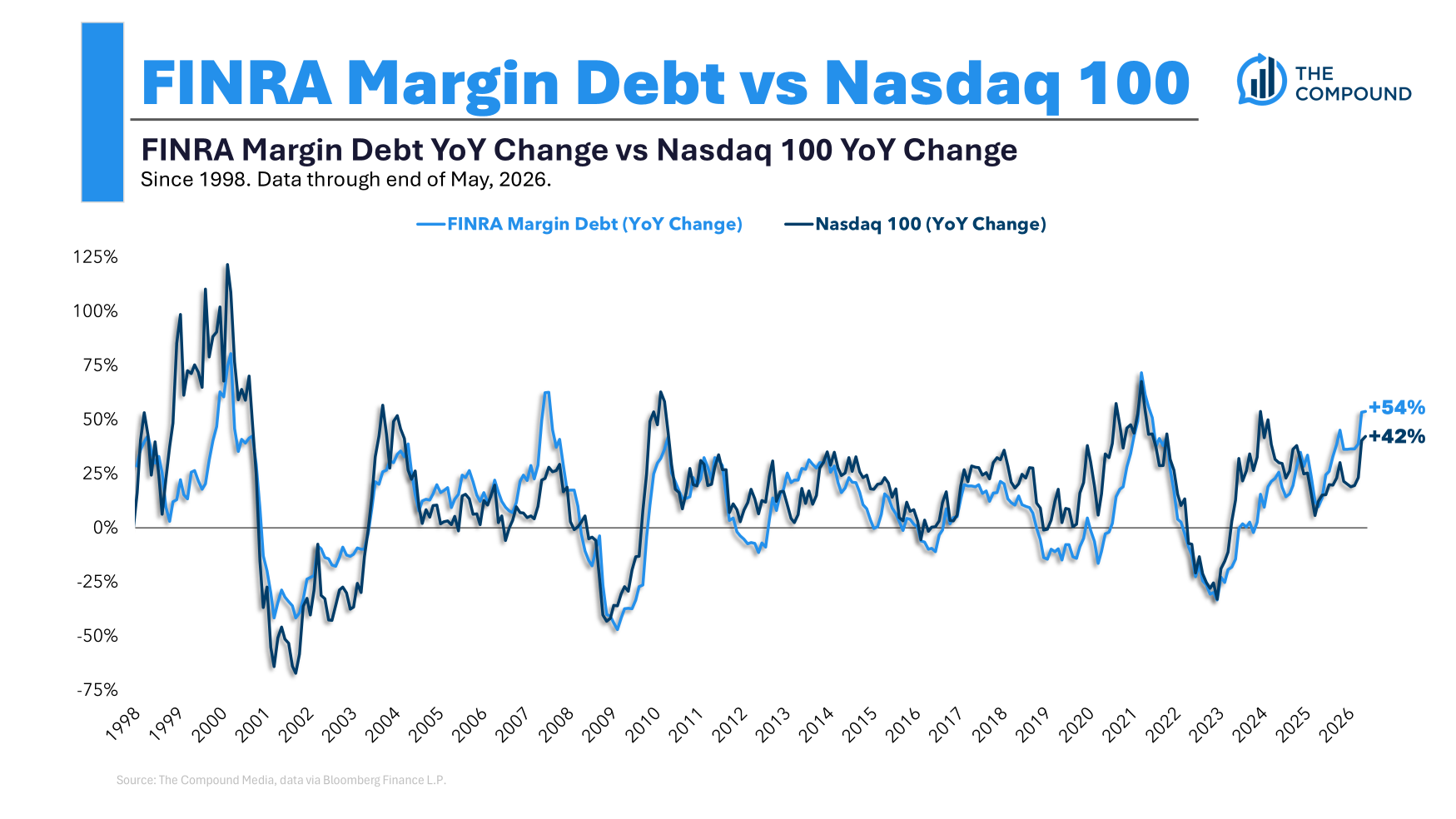

It makes sense that margin debt is at an all-time high because the stock market is at an all-time high. A simultaneous indicator:

Growth in margin debt tracks growth in the stock market:

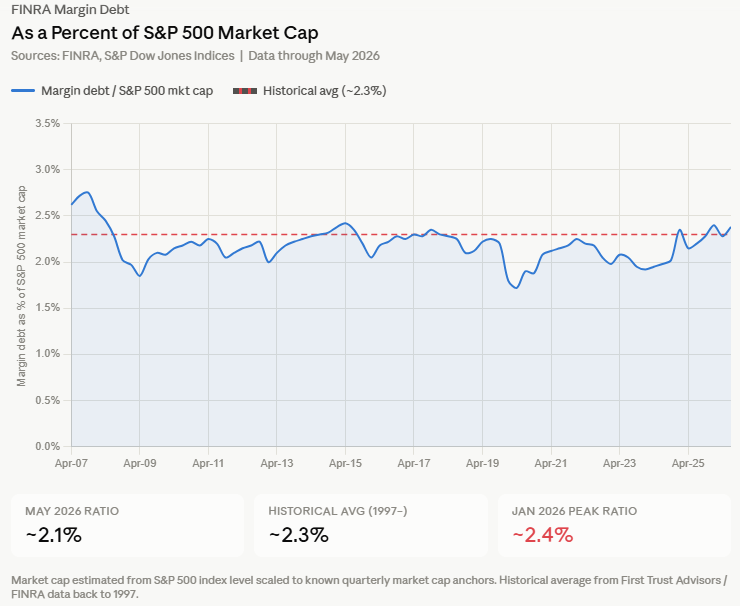

Now look at margin debt as a percentage of S&P 500 market cap:

Margin debt will not help you get to the top of the stock market. When the market falls, margin debt will also fall. If the market continues to rise, margin debt will continue to reach new highs.

However, SK Hynix, Samsung, Taiwan Semi, Micron, SanDisk, etc. I think the pressure on high-flying names such as will lead to some vacancies in these names.

These stocks are up between 150% and 700% this year alone. When you have such big gains packed into such a short period of time, it is inevitable that the huge up days will be interspersed with huge down days.

Add some leverage and big losses are sure to occur even if these stocks continue to rise.

That’s actually what happened in the 1987 crash. The stock market is up nearly 40% in the past year, heading into the pre-Black Monday slump.

Of course, I’m not saying this will happen to the general market.

It’s certainly possible that these stocks could cause some damage if sold. We will see.

All-time high-margin debt levels sound scary amid the tech boom. But all this tells you is that the market is also at all-time highs.

Debt can devastate individual investors who overextend themselves.

It would have to be much higher to push the market down.

Further Reading:

Two Things I Don’t Worry About

1It is worth noting that not all borrowings against stock portfolios return to the stock market. Sometimes it’s used for other things, too.