I wrote about a possible incident last week. Melt in Nasdaq 100.

This graphic is a good summary of that article:

Logical follow-up question (one many people ask): Is this a balloon?

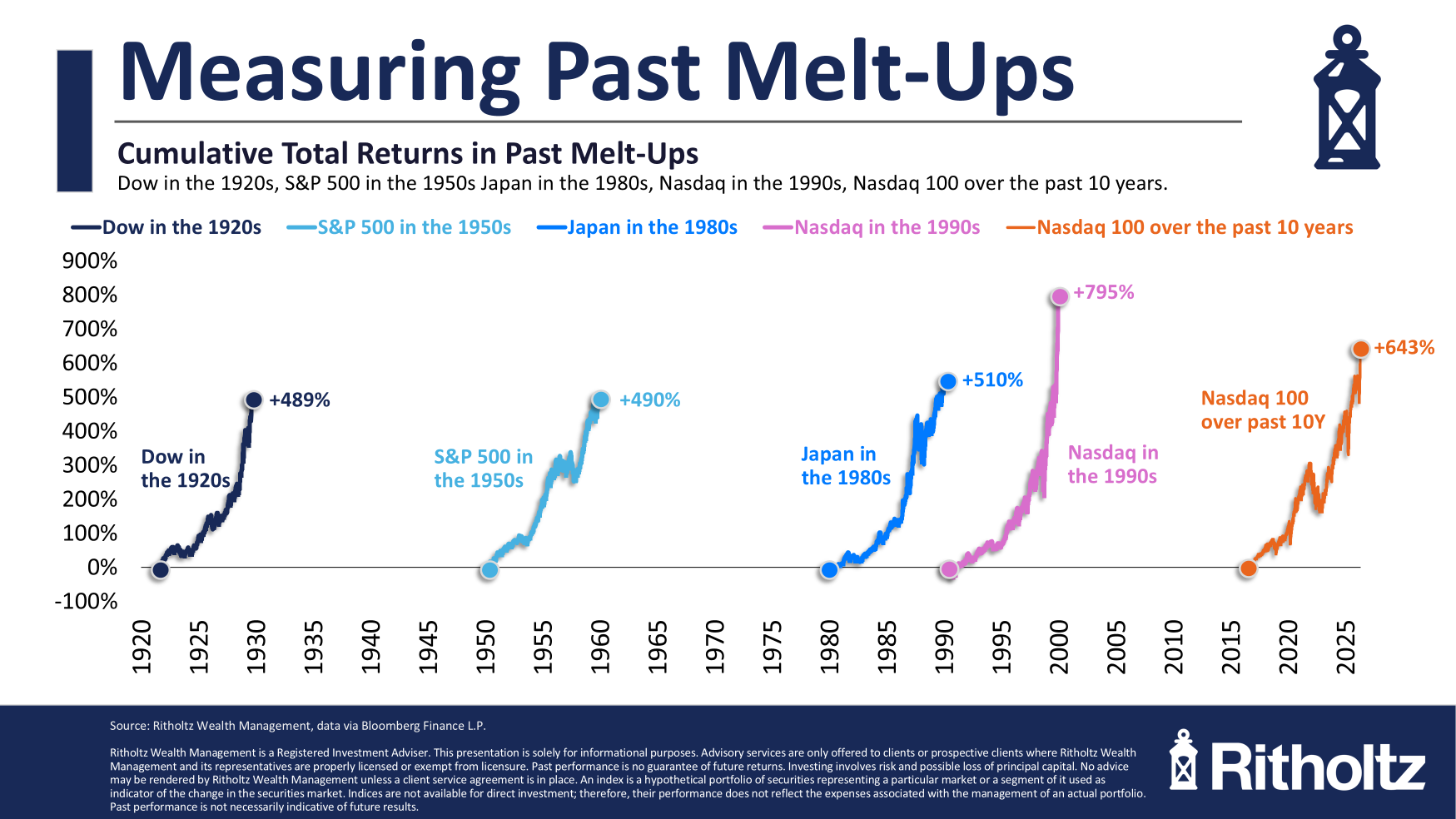

The Roaring 20s were a bubble. The 1950s were not a bubble. Japan was a bubble. The dot-com boom was a bubble.

This can be a difficult question to answer because everyone knows we’re in a financial crisis, but people aren’t very good at looking for bubbles.

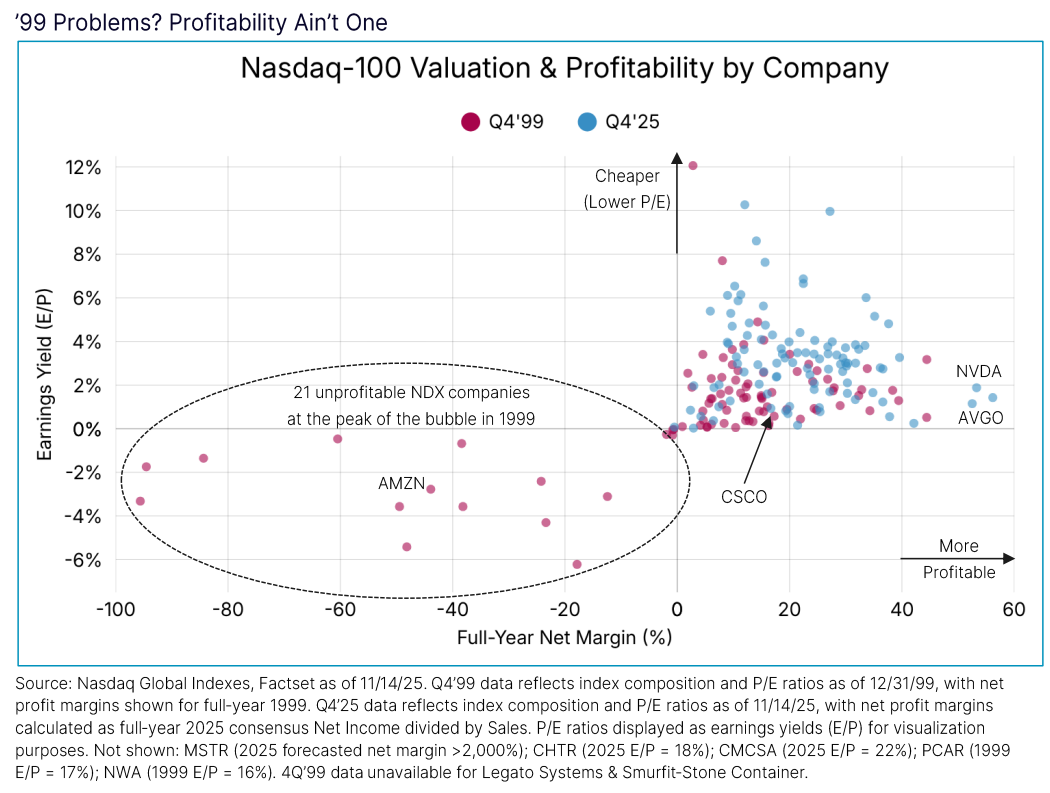

Many people assume this is the next dot-com bubble. They may be right. Let’s see. But it is worth comparing the two time periods to better understand the underlying fundamentals.

Nasdaq’s Mark Marex, “Is AI Another Bubble for Nasdaq 100?” Wrote a research article titled. looking for the answer to this question.

There were much more unprofitable companies at that time:

Today, companies are more profitable and have higher earnings returns.

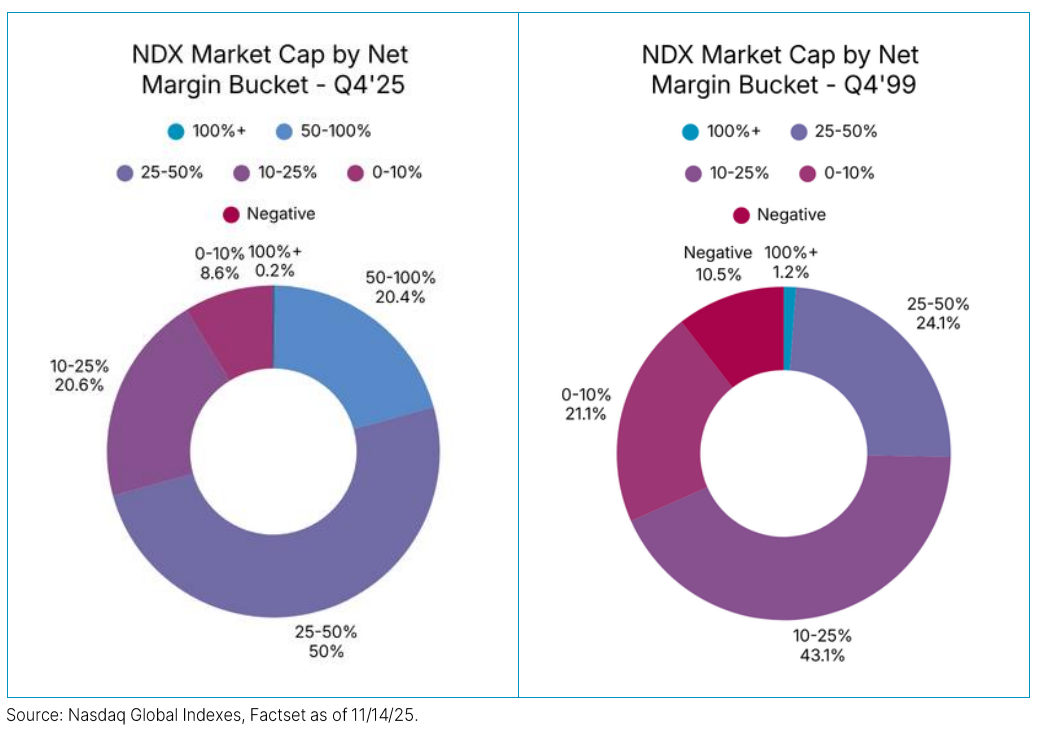

Today, too, margins are higher:

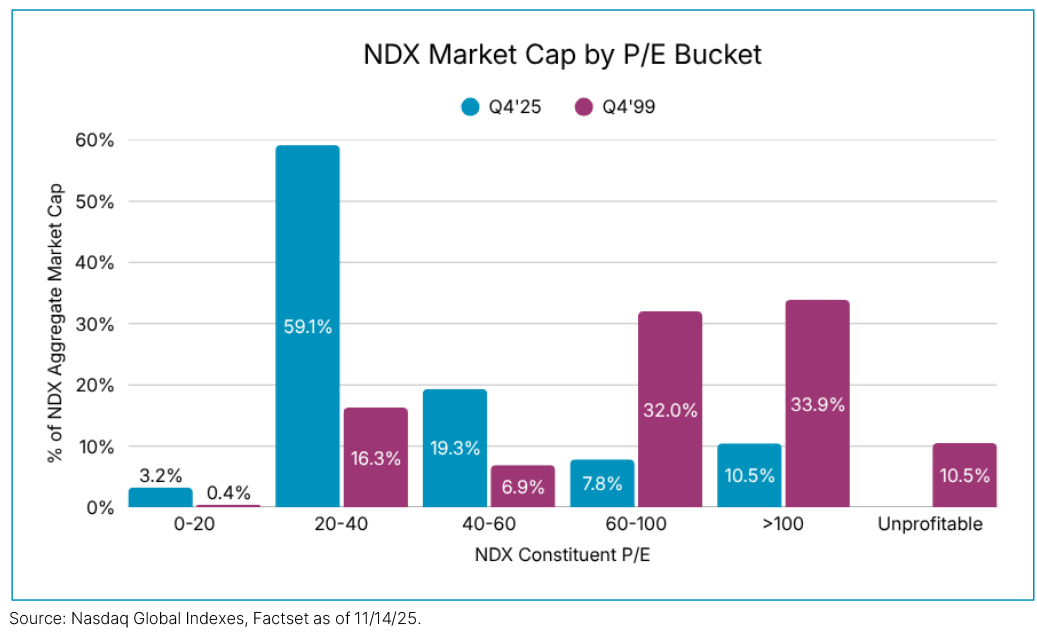

Considering the different P/E ratio buckets companies fall into compared to the late 1990s, valuations are much more reasonable today:

In 1999, more than 76% of stocks in the Nasdaq 100 had a P/E ratio of 60 times or higher. Today it is only 18% of the total.

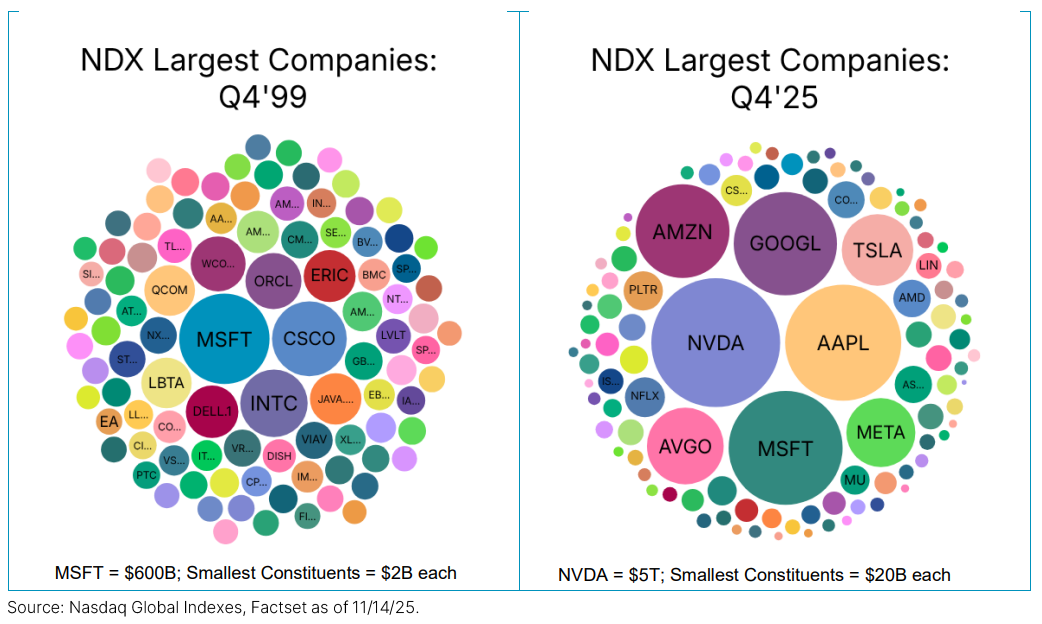

It wasn’t just a handful of tech stocks that were overvalued during the dot-com bubble. It was close to the entire tech stock market.

Right or wrong, good or bad, the questions are much more concentrated today than in 1999:

Most mega-cap tech companies have bought out the competition, so there’s more diversity than you might think.

Of course, it may not be fair to make comparisons with perhaps the biggest bubble in US stock market history.

Just because it doesn’t get any bigger than this the biggest The bubble does not prove that today is or is not a bubble. Maybe this is just a bubble on a smaller scale.

This is definitely possible.

But if this is a bubble, it is the most logical madness in history.

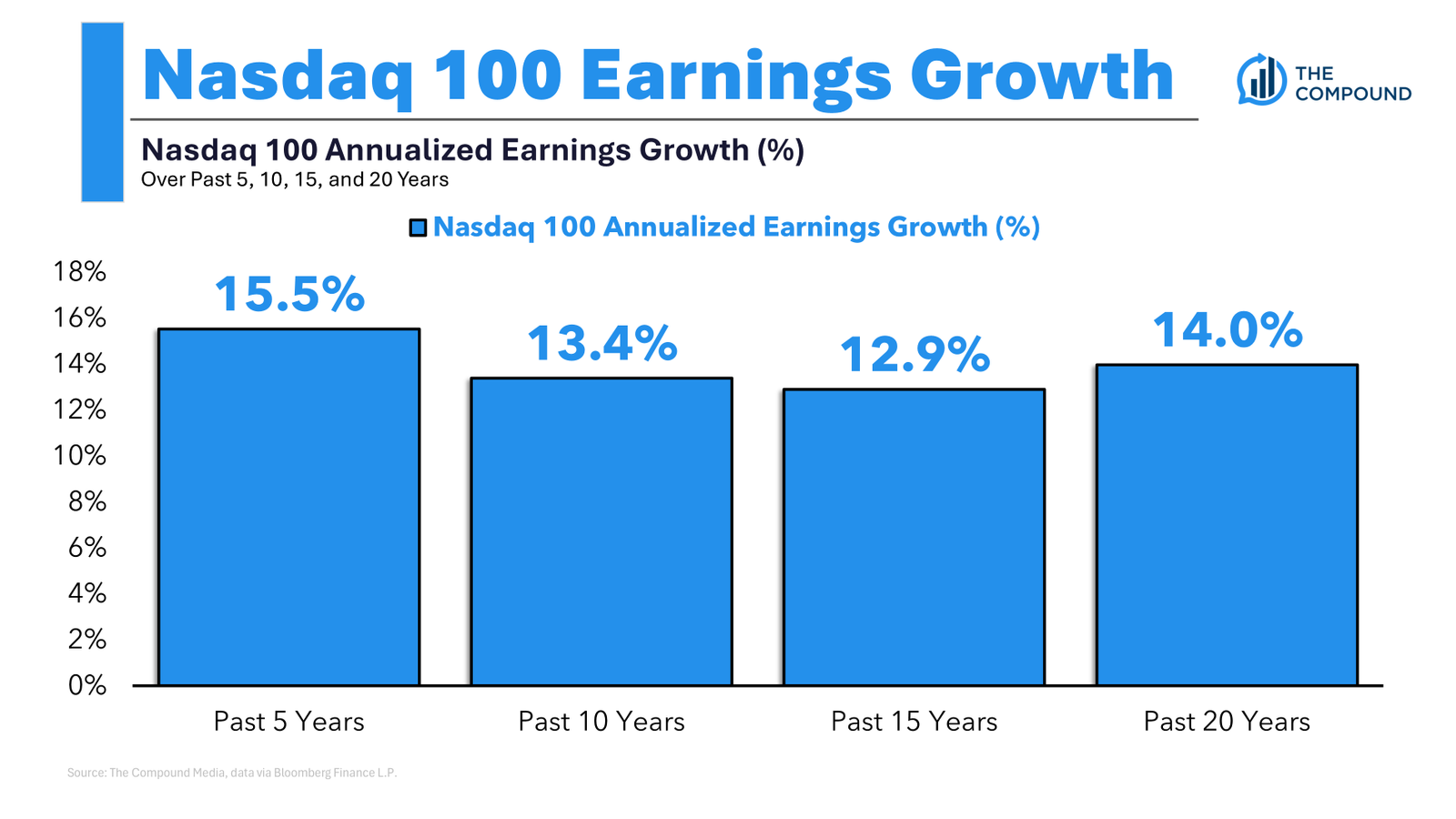

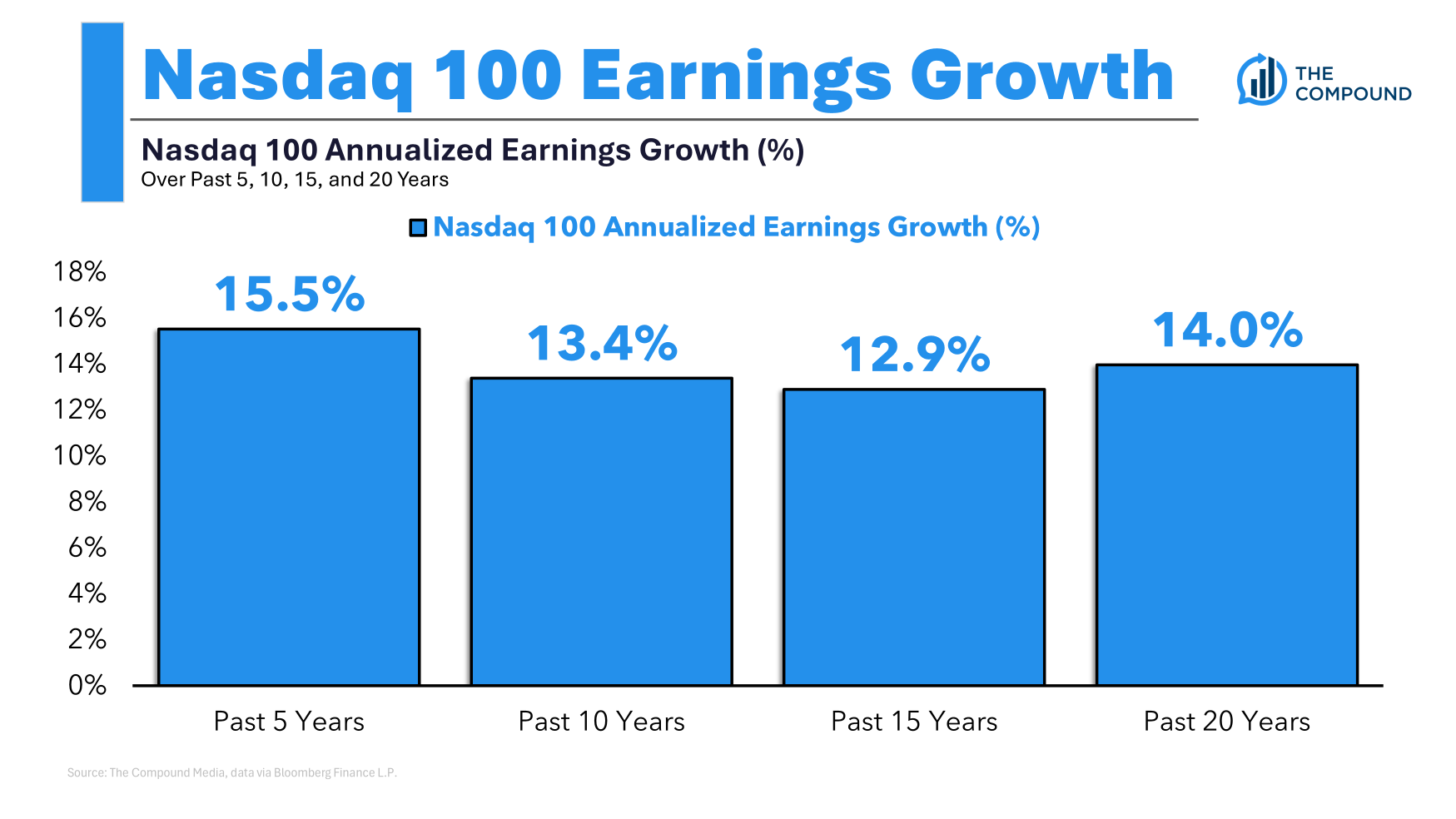

Look at the Nasdaq 100’s annual earnings growth going back 5, 10, 15 and 20 years:

Double-digit earnings growth over such a long period suggests fundamentals are starting to improve. Prices are not necessarily disconnected from reality.

Here are the annual Nasdaq 100 returns over the same time periods:

- Last 5 years +17.5%

- Last 10 years +21.9%

- Last 15 years +19.1%

- Last 20 years +16.3%

It’s not a perfect one-on-one relationship. But 14% annual earnings growth and 16% annual returns over the last 20 years are hard to beat.

Most asset bubbles involve suspension of disbelief when it comes to prices and fundamentals.

I’m not saying the market can’t fall. It can.

I’m not saying the market can’t crash. It can.

However, I say that this is one of the most difficult increases to prevent because earnings increase in parallel with prices.

This week on The Compound and Friends, we were talking tech stocks, valuations, AI and more with Josh, Michael and Kai Wu:

Further Reading:

Melting

This content containing security-related opinions and/or information is for informational purposes only and should in no way be relied upon as professional advice or endorsement of any practice, product or service. No guarantee or warranty can be given that the views expressed herein will apply to any particular case or circumstance and should not be relied upon in any way. You should consult your own advisors on legal, business, tax and other related matters regarding any investment.

The comments contained in this “post” (including any associated blogs, podcasts, videos, and social media) reflect the personal opinions, perspectives, and analyzes of Ritholtz Wealth Management employees making such comments and should not be considered the opinions of Ritholtz Wealth Management LLC. or its respective affiliates or a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any security or digital asset or performance data are for illustrative purposes only and do not constitute investment advice or an offer to provide investment advisory services. The tables and graphs contained therein are for informational purposes only and should not be taken into account when making any investment decisions. Past performance is not indicative of future results. The content speaks only from the date specified. Any projections, estimates, estimates, targets, expectations and/or opinions expressed in these materials are subject to change without notice and may differ from or contradict views expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives compensation from various organizations for advertising on affiliate podcasts, blogs and emails. The inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or Ritholtz Wealth Management or any of their employees. Investments in securities involve the risk of loss. For additional advertising disclaimers, see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see the descriptions Here.